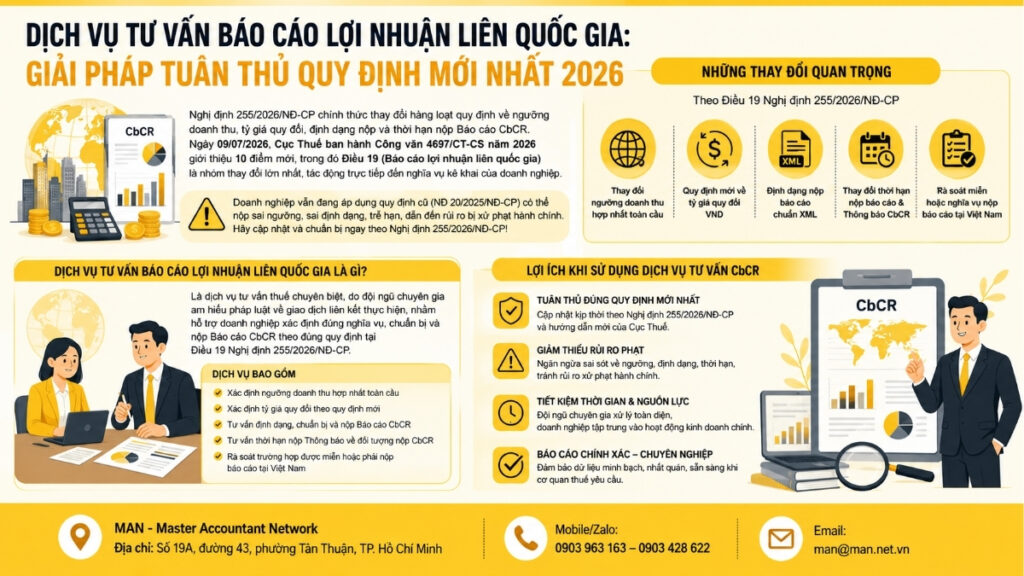

The Local File, a national document for related-party transactions, is mandatory but also poses the greatest risk during transfer pricing audits in 2026. This article provides a thorough and in-depth analysis of current legal regulations, clearly identifying who must prepare it, who is exempt, how to standardize FAR analysis, methods for comparing and determining safe profit margins, and warning of the risk of tax assessment, back taxes, and heavy penalties if the file is incorrectly prepared. The content is developed from an expert perspective on related-party transactions, helping businesses proactively control risks and optimize compliance even before the tax settlement period.

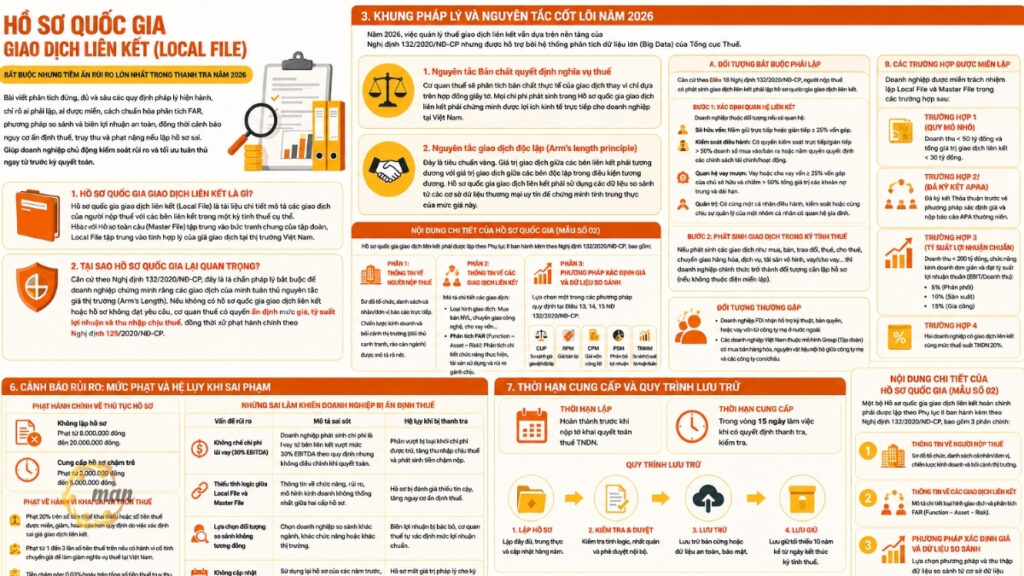

What is a country-specific related-party transaction profile?

The Local File (or Country File) is a detailed document describing the taxpayer's transactions with related parties during a specific tax period. Unlike the Master File, which focuses on the overall picture of the group, the Local File focuses on the reasonableness of the transaction prices in the Vietnamese market.

Why is national record important?

Based on Decree 132/2020/ND-CP, đây là lá chắn pháp lý bắt buộc để doanh nghiệp chứng minh rằng các giao dịch của mình tuân thủ nguyên tắc giá thị trường (Arm’s Length). Nếu không có hồ sơ quốc gia giao dịch liên kết hoặc hồ sơ không đạt yêu cầu, cơ quan thuế có quyền ấn định mức giá, tỷ suất lợi nhuận và thu nhập chịu thuế, đồng thời xử phạt hành chính theo Decree 125/2020/ND-CP.

Legal Framework and Core Principles 2026

Năm 2026, việc quản lý thuế giao dịch liên kết vẫn dựa trên nền tảng của Nghị định 132/2020/NĐ-CP nhưng được hỗ trợ bởi hệ thống phân tích dữ liệu lớn (Big Data) của Tổng cục Thuế.

Nguyên tắc Bản chất quyết định nghĩa vụ thuế

The tax authorities will analyze the actual nature of the transaction rather than relying solely on the paper contract. Any expenses incurred in the Country-Based Transfer Transaction File must demonstrate a direct economic benefit to the business in Vietnam.

Arm's length principle

This is the gold standard. The value of transactions between related parties must be equivalent to the value of transactions between independent parties under comparable conditions. Country records of related-party transactions must use comparative data from reputable trade databases to demonstrate the accuracy of these prices.

Detailed contents of the National Related-Party Transaction Profile (Form No. 02)

To ensure compliance, a complete national dossier on related-party transactions must be prepared according to the list in Appendix II issued with Decree 132/2020/ND-CP, including the following main sections:

Part 1: Taxpayer Information

Businesses need to provide an organizational chart and a list of individuals or units they report directly to. In particular, their business strategy and market context (competitors, industry barriers) need to be clearly described so that the tax authorities understand the company's position.

Part 2: Information about Related Party Transactions

This is the core part of the National Related-Party Transaction Profile. Businesses must describe:

- Types of transactions: Buying and selling raw materials, technology transfer, lending capital, etc.

- FAR (Function – Asset – Risk) analysis: A detailed analysis of the functions performed, assets used, and risks incurred.

Part 3: Pricing Methods and Comparative Data

The national dossier for related-party transactions must select one of the methods stipulated in Articles 13, 14, and 15 of Decree 132/2020/ND-CP:

- The Comparable Prices of Independent Transactions (CUP) method.

- Resale Price method.

- Cost Plus method.

- Phương pháp phân bổ lợi nhuận (PSM)

- Phương pháp so sánh tỷ suất lợi nhuận thuần (TNMM)

After understanding the structure and detailed content of the National Related-Party Transaction File (Form No. 02), the next question that most businesses are concerned about is: are they required to prepare the file, or are they exempt according to the law? Identifying the correct application from the outset not only helps businesses save on compliance costs but also avoids the risk of being misjudged during tax audits and inspections.

Download the Appendix II template for the National File on Related-Party Transactions:

Chi tiết đối tượng phải lập và các trường hợp miễn trừ

Identifying the right target helps businesses avoid unnecessary legal risks.

Entities required to create a National Related-Party Transaction Profile

According to Article 18 of Decree 132/2020/ND-CP, taxpayers with related-party transactions must prepare and maintain a National Related-Party Transaction File. To determine if they fall under this category, businesses need to go through two steps:

Step 1: Identify the business relationship that requires documentation if it has a relationship with the partner company, based on the following criteria:

- Capital ownership: One party directly or indirectly holds at least 25% of the other party's capital contribution.

- Operational control: One party has direct/indirect control over the total value of purchases/sales or has the power to decide on financial/operational policies.

- Lending relationship: The business borrows or lends at least 25% of the owner's equity and accounts for over 50% of the total value of the business's medium and long-term debts.

- Management: Having a single individual who runs, controls, or is jointly managed by a group of individuals who are related by family ties.

Step 2: Transactions occur during the tax period. After determining the relationship between the two parties, if transactions such as buying, selling, exchanging, leasing, renting, transferring goods, services, intangible assets, borrowing/lending, etc., arise, the business officially becomes subject to the requirement of completing the necessary documentation. hồ sơ xác định giá giao dịch liên kết (nếu không thuộc diện miễn lập hồ sơ giao dịch liên kết).

Specific target groups commonly encountered:

- FDI enterprises receive technical support, intellectual property rights, or loans from their parent companies abroad.

- Vietnamese businesses operating under the Group model engage in internal buying and selling of goods and raw materials between the parent company and its subsidiaries/subsidiaries.

Cases exempt from national related-party transaction filing.

Businesses are exempt from the responsibility of creating Local Files and Master Files in the following cases:

- Case 1 (Small scale): Revenue below VND 50 billion and total value of related-party transactions below VND 30 billion;

- Case 2 (APA Signed): A Pre-Agreement on Pricing Methodology has been signed and annual APA reports have been submitted.

- Case 3 (Standard Profit Margin): Revenue below VND 200 billion, performing simple business functions and achieving a net profit margin (EBIT/Revenue) of 5% (Distribution), 10% (Manufacturing) or 15% (Processing);

- Case 4: Two businesses have related-party transactions with the same corporate income tax rate under Article 20%.

Mặc dù quy định đã phân định rõ đối tượng phải lập và các trường hợp được miễn trừ Hồ sơ quốc gia giao dịch liên kết nhưng trên thực tế, không ít doanh nghiệp hiểu sai điều kiện miễn, áp dụng không đầy đủ hoặc không chứng minh được căn cứ pháp lý khi bị kiểm tra. Đây chính là nguyên nhân khiến nhiều hồ sơ bị bác bỏ, dẫn đến truy thu và xử phạt nặng. Từ đây, doanh nghiệp cần đặc biệt lưu ý đến các rủi ro, mức phạt và hệ lụy pháp lý khi vi phạm quy định về giao dịch liên kết trong các kỳ thanh tra thuế.

Reference: Dịch vụ lập hồ sơ giao dịch liên kết.

Cảnh báo rủi ro: Mức phạt và hệ lụy khi sai phạm Hồ sơ quốc gia giao dịch liên kết

In 2026, the Tax Authority will not only collect back taxes but also apply strict penalties according to Decree 125/2020/ND-CP. Deficiencies in the National Related-Party Transaction Record can cause businesses to face:

Administrative penalties for procedural issues.

For violations related to the establishment and provision of documentation, businesses will be subject to direct administrative sanctions, specifically as follows:

- Failure to prepare documentation: A fine of VND 8,000,000 to VND 20,000,000 will be imposed for the act of failing to prepare documentation for determining the transfer pricing of related-party transactions as required by regulations.

- Late submission of documents: A fine of VND 2,000,000 to VND 5,000,000 will be imposed if documents are submitted late compared to the deadline required by the inspection agency or if the required list of documents is incomplete.

Penalties for false declarations and tax evasion.

However, the aforementioned administrative penalties are merely the tip of the iceberg. The most severe financial consequences lie in the sanctions directly applied to the amount of tax payable when a business is found to have committed pricing violations:

- Penalties under Article 20% apply to the amount of underdeclared tax or the amount of tax exempted, reduced, or refunded in excess of regulations due to incorrect determination of transfer pricing.

- A penalty of 1 to 3 times the amount of tax evaded will be imposed if the tax authorities determine that the enterprise intentionally engaged in transfer pricing to reduce its tax obligations in Vietnam.

- Tiền chậm nộp: Tính 0.03%/ngày trên tổng số tiền thuế truy thu. Đây là con số lãi chồng lãi cực kỳ nguy hiểm nếu đợt thanh tra kéo dài qua nhiều kỳ tính thuế.

The authority to determine taxes

The tax authorities have the right to determine the profit margin if a valid country record of related-party transactions is not provided.

Những sai lầm khiến doanh nghiệp bị ấn định thuế

To help businesses quickly identify common errors and proactively prevent audit risks, the table below summarizes typical issues arising during the preparation of the National Related-Party Transaction File, along with the practical consequences when tax authorities conduct audits and assess taxes.

| Risk issues | Describe the error. | Consequences of being inspected |

| Control interest expense (30% EBITDA) | The company incurred interest expense from related parties exceeding the 30% EBITDA limit as stipulated but did not adjust it during tax settlement. | The excess amount is disallowed as a deductible expense, increasing taxable income and resulting in late payment penalties. |

| There is a lack of logical connection between Local Files and Master Files. | Information regarding functionality, risks, and business model is inconsistent between the two levels of documentation. | The file was deemed unreliable, increasing the risk of tax assessment. |

| Choose dissimilar objects for comparison. | Businesses select comparable businesses from different industries, different functions, or different markets. | The profit margin was rejected, and the tax authorities determined the standard profit margin themselves. |

| No annual record updates | Reusing records from previous years, without updating financial data and business context. | The records are legally invalid for the tax period under audit. |

| Demonstrate the usefulness of internal services. | Lack of actual service evidence; inability to demonstrate economic benefits received. | The service fee was excluded (100%), increasing the corporate income tax payable. |

Errors in the Local File (National File for Related-Party Transactions) often don't stem from intentional violations but rather from misunderstanding regulations, lack of updates, and superficial preparation of the file. However, in the context of increasingly thorough tax audits, these errors can lead to the exclusion of expenses, tax assessments, and significant penalties, forcing businesses to proactively review and complete their files systematically and consistently from the beginning of the tax period.

Để tránh những rủi ro đáng tiếc có thể xảy ra, doanh nghiệp nên chủ động tham vấn dịch vụ tư vấn giao dịch liên kết từ các đơn vị uy tín, chuyên sâu và có kinh nghiệm như MAN – Master Accountant Network để được tư vấn và hỗ trợ chuyên sâu, đúng lĩnh vực và quy mô cua doanh nghiệp.

Delivery time and storage procedures

Based on Article 18 of Decree 132/2020/ND-CP:

- Deadline for preparation: To be completed before submitting the corporate income tax return.

- Thời hạn cung cấp: Trong vòng 15 ngày làm việc khi có quyết định thanh tra kiểm tra.

Conclude

National related-party transaction records are no longer simply a compliance obligation but have become a tool to protect businesses from the risk of prolonged tax assessments and retroactive tax collection. As the Tax Authority intensifies data analysis and targeted audits in 2026, standardizing records, selecting appropriate pricing methods, and updating information promptly will help businesses proactively control tax costs and maintain financial transparency. In cases where businesses need to review compliance levels or prepare records before an audit, consulting with related-party transaction experts early on will be an effective step to minimize risks.

Standardizing the national transfer pricing documentation from the outset will help businesses avoid the risks of prolonged tax assessments and collection delays. If your business needs independent review of Local File and Master File or preparation of documentation before an audit, the support of MAN – Master Accountant Network, with its team of experienced transfer pricing experts, will help make the compliance process more systematic, efficient, and cost-effective.

Liên hệ MAN – Master Accountant Network đê được hỗ trợ và tư vấn miễn phí!

Contact information MAN – Master Accountant Network

- Address: No. 19A, Street 43, Tan Thuan Ward, Ho Chi Minh City

- Mobile/Zalo: 0903 963 163 – 0903 428 622

- E-mail: man@man.net.vn

Content production by: Mr. Le Hoang Tuyen – Founder and CEO of MAN – Master Accountant Network, CPA Vietnam with over 30 years of experience in accounting, auditing, and financial consulting.

Frequently Asked Questions about the Country Profile for Related-Party Transactions

Không. Doanh nghiệp không phải nộp hồ sơ quốc gia cùng tờ khai quyết toán thuế TNDN mà phải lập, hoàn thiện và lưu trữ trước thời điểm nộp quyết toán. Hồ sơ chỉ xuất trình khi cơ quan Thuế yêu cầu thanh tra, kiểm tra và thời hạn cung cấp thường là 15 ngày làm việc theo quy định.

Doanh nghiệp có thể được miễn lập Local File nếu thuộc một trong các trường hợp như: Doanh thu dưới 50 tỷ đồng và giao dịch liên kết dưới 30 tỷ đồng; Đã ký APA; Doanh thu dưới 200 tỷ đồng và đạt tỷ suất lợi nhuận chuẩn; hoặc giao dịch giữa các bên cùng thuế suất TNDN theo quy định.

Có. Việc doanh nghiệp lỗ nhiều năm không phải là căn cứ miễn lập Local File. Ngược lại, doanh nghiệp liên tục báo lỗ nhưng vẫn phát sinh giao dịch liên kết thường là nhóm bị cơ quan Thuế kiểm tra trọng điểm vì có rủi ro cao liên quan đến chuyển giá và điều chỉnh lợi nhuận.

Có rủi ro rất lớn. Hồ sơ quốc gia giao dịch liên kết phải được hoàn thiện trước thời điểm nộp quyết toán thuế TNDN. Việc lập hồi tố sau khi có quyết định thanh tra thường bị đánh giá là không hợp lệ, dễ dẫn đến ấn định thuế, truy thu và xử phạt hành chính nghiêm trọng.

Phân tích FAR (Functions - Assets - Risks) là phần quan trọng nhất để xác định bản chất giao dịch liên kết. Cơ quan Thuế dựa vào để đánh giá doanh nghiệp thực hiện chức năng gì, sử dụng tài sản nào và chịu rủi ro ra sao, từ đó xác định mức lợi nhuận phù hợp theo nguyên tắc giao dịch độc lập.

Các nội dung thường bị kiểm tra sâu gồm: Chi phí dịch vụ nội bộ, phí bản quyền, lãi vay liên kết, phân tích FAR, lựa chọn doanh nghiệp so sánh và biên lợi nhuận. Nếu doanh nghiệp không chứng minh được tính hợp lý và lợi ích kinh tế thực tế, cơ quan Thuế có thể loại chi phí và truy thu thuế.Hồ sơ quốc gia giao dịch liên kết có bắt buộc nộp cùng tờ khai quyết toán thuế TNDN không?

Doanh nghiệp được miễn lập Hồ sơ quốc gia giao dịch liên kết khi nào?

Doanh nghiệp lỗ nhiều năm có bắt buộc lập Hồ sơ quốc gia giao dịch liên kết không?

Nếu lập hồ sơ quốc gia sau thời điểm quyết toán thuế thì có bị xử phạt không?

Phân tích FAR trong Hồ sơ quốc gia giao dịch liên kết có vai trò gì?

Cơ quan Thuế thường kiểm tra nội dung nào nhiều nhất trong Local File?