Giao dịch liên kết Nghị định 132 là một trong những mảng thuế phức tạp nhất, ảnh hưởng trực tiếp đến nghĩa vụ thuế thu nhập doanh nghiệp (TNDN) và rủi ro chuyển giá. Từ việc xác định bên liên kết, phân tích chức năng, tài sản và rủi ro (FAR Analysis), đến lựa chọn phương pháp xác định giá thị trường. Mọi bước đều đòi hỏi sự chính xác tuyệt đối và tuân thủ theo Decree 132/2020/ND-CP.

Bài viết dưới đây tổng hợp toàn bộ quy định trọng yếu, hướng dẫn triển khai, các nghĩa vụ kê khai, lập hồ sơ và kinh nghiệm thực tiễn giúp doanh nghiệp giảm thiểu rủi ro thanh tra, tối ưu thuế và đảm bảo tuân thủ pháp luật. Trong trường hợp doanh nghiệp cần hỗ trợ chuyên sâu, việc tham khảo dịch vụ tư vấn giao dịch liên kết sẽ giúp đánh giá rủi ro và xây dựng phương án tuân thủ hiệu quả hơn.

What is affiliate trading? Understanding its nature

Giao dịch liên kết Nghị định 132 không phải là giao dịch mua bán thông thường. Đó là các giao dịch phát sinh giữa hai hay nhiều bên có mối quan hệ sở hữu, kiểm soát hoặc điều hành lẫn nhau.

Bản chất của giao dịch liên kết Nghị định 132 là do các bên không hành động độc lập, giá cả và điều kiện giao dịch có thể bị điều chỉnh để đạt mục tiêu kinh tế, phổ biến nhất chính là chuyển lợi nhuận sang khu vực có thuế suất thấp hơn (hay còn gọi là chuyển giá).

Điểm khác biệt giữa giao dịch bình thường và giao dịch liên kết theo Nghị định 132

Sự khác biệt giữa giao dịch liên kết Nghị định 132 và giao dịch bình thường là nếu doanh nghiệp mua hàng từ một đối tác độc lập, giá sẽ được xác định theo cung – cầu thị trường.

Tuy nhiên nếu doanh nghiệp mua từ công ty mẹ, giá có thể được định ở mức cao hơn (để giảm lợi nhuận của công ty con ở Việt Nam) hoặc thấp hơn (cho mục đích khác). Chính sự khác biệt này khiến cho giao dịch liên kết Nghị định 132 trở thành đối tượng quản lý chặt chẽ.

Vì sao các doanh nghiệp phát sinh giao dịch liên kết cần tuân thủ chặt chẽ Nghị định 132/2020/NĐ-CP?

In fact, Decree 132 sets out two core responsibilities that every business with related-party transactions cannot ignore, namely:

- Nghĩa vụ Kê khai và Lập Hồ sơ: Doanh nghiệp bắt buộc phải kê khai các giao dịch này và trong nhiều trường hợp, phải lập Transfer pricing determination dossier.

- Risk of Audits and Tax Collection: If the tax authorities discover that the transfer pricing does not comply with the arm's length principle, the business will have its taxable income adjusted upwards, leading to the collection of corporate income tax and administrative penalties.

Vậy, làm thế nào để doanh nghiệp có thể quản lý và giảm thiểu những rủi ro thuế TNDN và tránh bị điều chỉnh thu nhập chịu thuế? Bước đi đầu tiên và mang tính nền tảng quyết định toàn bộ quá trình tuân thủ giao dịch liên kết Nghị định 132, chính là việc xác định đúng và đủ ai là Bên liên kết và giao dịch nào được coi là Giao dịch liên kết theo quy định tại Khoản 2 Điều 5 Nghị định 132/2020/NĐ-CP.

Xác định Bên liên kết và Giao dịch liên kết Nghị định 132

Để tuân thủ đúng quy định về giao dịch liên kết Nghị định 132, bước đầu tiên quan trọng nhất là xác định chính xác ai là Bên liên kết và giao dịch nào là giao dịch liên kết.

Portrait of the Affiliate as prescribed in Decree 132

Việc xác định Bên liên kết được quy định chi tiết và đầy đủ tại Khoản 2 Điều 5 Nghị định 132. Dưới đây là các trường hợp cụ thể:

- An enterprise directly or indirectly holds at least 25% of the equity of the owner of the other enterprise.

- Both enterprises have at least 25% of owner's equity held directly or indirectly by a third party.

- Doanh nghiệp chịu sự điều hành, kiểm soát về mặt quyết định kinh doanh hoặc tài chính bởi một cá nhân hoặc tổ chức, hoặc cá nhân hoặc tổ chức này có quyền chỉ định đa số thành viên Ban lãnh đạo của hai doanh nghiệp.

- Two companies have more than 50% members of the Board of Directors (Board of Members, etc.) appointed by the same third party, or have family relationships (spouse, parents, children, siblings) between key members.

- Two businesses must have at least one person holding a key management position (e.g., Director, General Director, Deputy Director, etc.) or having a significant influence on business or financial decision-making.

- One business lends capital to another business in any form (including guarantees), provided that the loan represents at least 25% of the owner's equity and exceeds 50% of the total value of the borrower's operating assets.

- One business provides goods or services exclusively to another business, or together they control the consumer market or supply source through an agreement.

- Một bên sử dụng, bán, hoặc chuyển giao công nghệ, nhãn hiệu thương mại, quyền sở hữu trí tuệ của bên kia; hoặc cả hai bên đều chịu sự kiểm soát về công nghệ hoặc nhãn hiệu bởi bên thứ ba.

- One party has the right to appoint members of the Board of Directors, the Management Board, or other management positions that have the authority to determine the other party's business policies.

- Hai doanh nghiệp có mối quan hệ quyết định hoặc cùng quyết định các điều kiện của giao dịch phát sinh giữa các bên.

- One party engages in purchase, sale, or exchange transactions with the other party that account for 50% of the total value of goods and services generated by each party during the tax period (applicable in cases where the transaction does not comply with the principle of independence).

Important Note: Nghị định 132 áp mức 25% vốn góp là ngưỡng cứng để xác định quan hệ liên kết trong các trường hợp. Việc rà soát cơ cấu sở hữu vốn tại thời điểm cuối kỳ tính thuế là bắt buộc. Trường hợp về vay vốn là một trong những tiêu chí phức tạp và dễ dẫn đến rủi ro chuyển giá nhất.

Phân loại các loại giao dịch liên kết Nghị định 132 phổ biến

Bất kỳ giao dịch nào phát sinh giữa các Bên liên kết đều là giao dịch liên kết và đều chịu sự điều chỉnh của Nghị định 132/2020/NĐ-CP. Các loại giao dịch liên kết Nghị định 132 phổ biến bao gồm:

| Affiliated trading group | Transaction details | Note |

| Financial Affiliate Transactions | Borrowing or lending capital between related parties Loan guarantee Providing debt instruments | Directly related to the 30% EBITDA interest expense limit under Article 16 of Decree 132. |

| Commercial affiliate transactions | Buying and selling goods Purchasing raw materials and finished products. Providing or renting services (excluding financial and banking services). | The most common type of related party transaction, usually using the CUP, RPM or TNMM method. |

| Invisible Affiliate Transactions | Transfer of rights to use or ownership of intangible assets (brands, technology, copyrights) Royalty Fee Management fee. | This group is most at risk of being audited by tax authorities because it is difficult to determine market value. |

| Internal link transactions | Sharing corporate management costs Headquarter Costs Internal support services | The business must demonstrate that it has received a real benefit and charge on the independence principle. |

Related transactions in enterprises are not only diverse in form but also clearly different in complexity and tax risks. In particular, Financial related transactions are often subject to the strictest supervision due to their direct impact on interest expenses according to Article 16 of Decree 132/2020/ND-CP. In addition, commercial, intangible and internal service transactions all require enterprises to have a complete valuation dossier, proving the nature and value of the transaction in accordance with the independence principle to minimize tax risks and comply with the law.

Methods for determining transfer pricing Decree 132

Mục tiêu cốt lõi của giao dịch liên kết Nghị định 132 là đảm bảo giá các giao dịch liên kết phải được xác định dựa trên nguyên tắc giá thị trường độc lập (Arm’s Length). Để làm được điều đó, doanh nghiệp phải lựa chọn và áp dụng phương pháp xác định giá phù hợp.

Principles for Determining the Independent Market Price (Arm's Length)

Để chứng minh giao dịch liên kết được thực hiện như giao dịch độc lập, doanh nghiệp phải tìm các giao dịch tương đương giữa các bên không liên kết và so sánh các điều kiện kinh tế, tài chính của chúng.

The criteria for selecting comparison objects are as follows:

- So sánh giao dịch độc lập nội bộ: Tức là giao dịch tương tự mà chính doanh nghiệp thực hiện so sánh với một bên thứ ba độc lập.

- Compare independent external transactions: Similar transactions between two other independent third parties.

Comparisons must ensure similarity in terms of Function, Assets, Risk (FAR Analysis), contractual conditions, economic conditions, and business strategies.

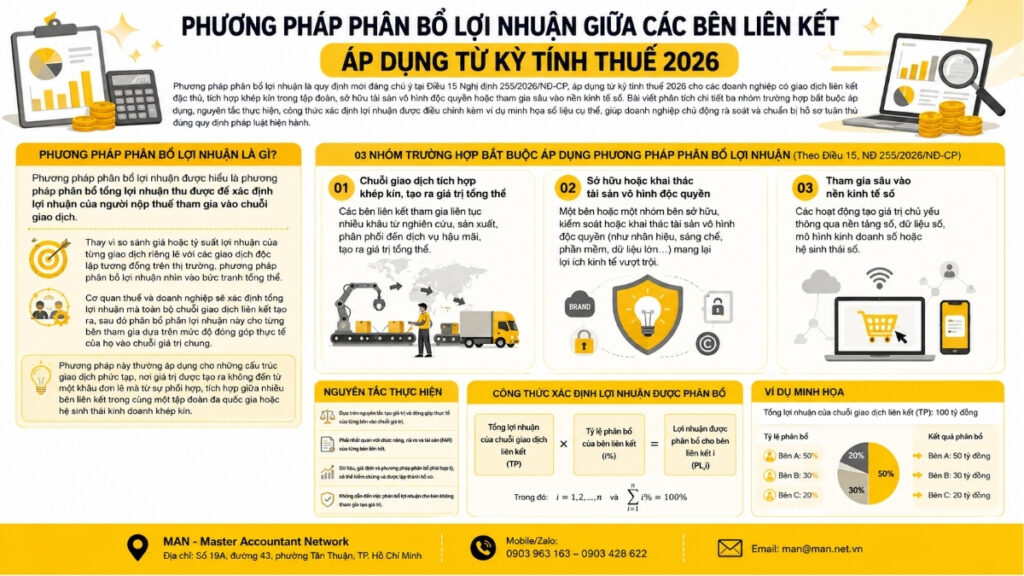

Ứng dụng 05 phương pháp xác định giá giao dịch liên kết Nghị định 132

Nghị định 132/2020/NĐ-CP quy định 05 phương pháp cơ bản, được phân loại thành phương pháp truyền thống và phương pháp lợi nhuận:

| Method | Mainly applied | Principle |

| Compare Independent Transaction Prices (CUP) | Trading similar goods and services. | Compare the selling price of the product of the related transaction with the price of similar products between independent parties. |

| Resale Price (RPM) | Distribution and trading businesses create little added value. | Take the resale price to the independent party minus the independent gross profit margin. |

| Cost plus profit (CPM) | Manufacturing, processing and service providing enterprises. | Add an independent gross profit margin to the cost of production or service provision of the associated transaction. |

| Net Profit (NPP) | Popular for many types of affiliate deals. | Compare the net profit margin (on revenue, costs, assets) of the related transaction with the independent net profit margin. |

| Profit Distribution Metric (PSM) | Affiliated transactions are unique and create intangible assets. | Divide the total profit earned from the related party transaction according to the contribution ratio of each party. |

Choosing which method to use to determine the transfer pricing under Decree 132 is a complex process. Businesses need to conduct Functional Analysis (FAR) to determine their role (purely manufacturing, distributing low risk, or holding high risk).

Nghĩa vụ kê khai và Lập Hồ sơ xác định giá

Compliance with the regulations on related party transactions of Decree 132 is demonstrated through two main obligations: Declaration and Documentation.

Kê khai giao dịch liên kết hàng năm

Các doanh nghiệp có phát sinh giao dịch liên kết trong kỳ tính thuế đều bắt buộc phải kê khai thông tin về giao dịch liên kết và các bên liên kết trong Hồ sơ khai thuế TNDN kèm theo Related Party Transaction Appendix, ngay cả khi họ được miễn lập Hồ sơ Xác định Giá.

- Biểu mẫu bắt buộc: Doanh nghiệp sử dụng Mẫu 01 (Phụ lục giao dịch liên kết kèm theo Tờ khai Quyết toán TNDN).

- Important details: Form 01 requires the declaration of the total value of related-party transactions, the relationship between the two parties, the pricing method, and especially interest expense (to control the limit according to Article 16). Declaring Form 01 is the first step for the Tax Authority to assess the transfer pricing risk of the enterprise.

See details: Declare related party transactions on HTKK

Components of the Transfer Pricing Documentation

The transfer pricing documentation is legal evidence proving that the related transactions of an enterprise are carried out according to the independent market principle. This documentation includes 03 levels.

| File | Condition | Content |

| Local File | Required for all businesses with related transactions. | Information about business, industry, business strategy. Describe in detail each related transaction that occurs. Functional analysis (FAR) of the enterprise and its related parties. Analysis, comparison and selection of methods for determining transfer pricing. Calculate price adjustments (if necessary). |

| Master File | Applicable to businesses that are members of multinational corporations. The Group's global consolidated revenue is over VND 10,000 billion. | Overview of the Group's ownership structure. Global business operations. The Group's general transfer pricing policy. |

| Country-Based Profit and Loss Report (CbCR) | Applicable to multinational corporations with total global consolidated revenue of over VND 18,000 billion. | Summary information on revenue distribution. Profit, tax paid in each country. Business activities between countries. |

The three levels of related party transaction records above show the increasing level of transparency that enterprises must meet when participating in multinational corporations. In particular, Local File is a mandatory obligation for most enterprises with related party transactions, while Master File and CbCR only apply when the Group's consolidated revenue reaches the threshold according to Decree 132. The full and timely preparation of these Records not only helps enterprises comply with the law but also reduces the risk of tax collection, tax assessment and increases transparency in operations.

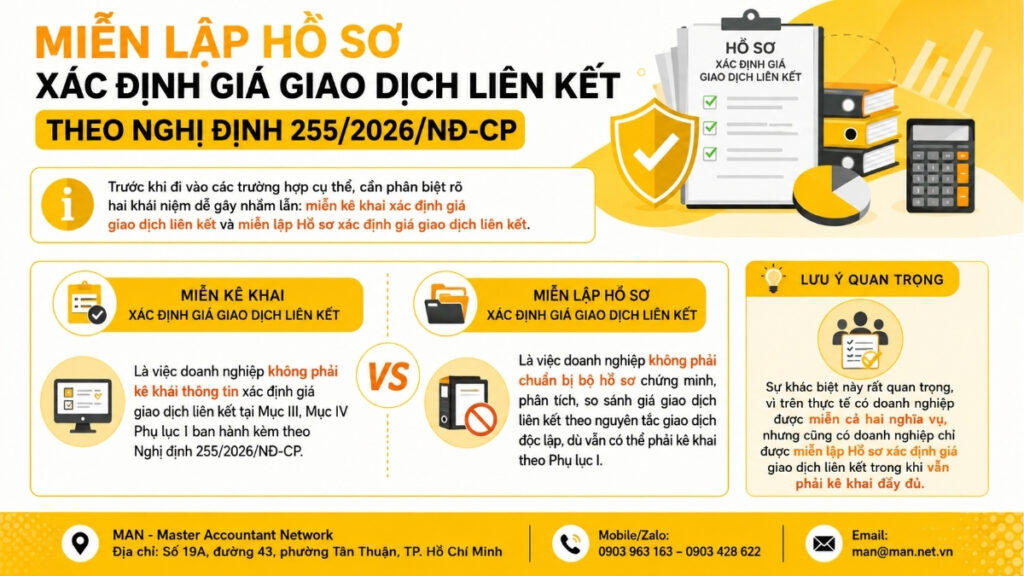

Cases exempted from preparing price determination dossiers

Nghị định 132/2020/NĐ-CP cung cấp các điều kiện cụ thể để doanh nghiệp được miễn lập Hồ sơ xác định giá, giúp giảm gánh nặng tuân thủ cho các doanh nghiệp nhỏ hoặc có rủi ro chuyển giá thấp.

Doanh nghiệp được miễn nếu đáp ứng một trong các điều kiện sau:

Điều kiện về Quy mô và Giá trị Giao dịch

Đáp ứng đồng thời cả 02 điều kiện:

- Total revenue generated during the tax period is less than 50 billion VND;

- Total value of all related transactions arising in the tax period is under 30 billion VND.

Điều kiện về Hiệu lực Thỏa thuận trước về Phương pháp xác định giá tính thuế (APA)

The Enterprise has signed an Advance Pricing Agreement (APA) and continues to comply with this Agreement.

Điều kiện về tỷ suất lợi nhuận và thực hiện chức năng đơn giản

- Thứ nhất, doanh nghiệp chỉ phát sinh giao dịch với các bên liên kết là đối tượng nộp thuế TNDN tại Việt Nam;

- Second, apply the same corporate income tax rate as the related party (i.e. there is no difference in tax rates);

- Thứ ba, cả hai bên liên kết đều không được hưởng ưu đãi thuế TNDN trong kỳ tính thuế;

- Fourth, total revenue generated during the tax period is less than 200 billion VND;

- Fifth, apply the net profit margin before interest and corporate income tax on net revenue, after deducting interest expenses and non-deductible expenses as prescribed for distribution from 5% or more, for production from 10% or more and for processing from 15% or more.

Even if exempted from preparing a Profile, the enterprise must still:

- Kê khai đầy đủ thông tin về giao dịch liên kết vào Mẫu 01 (Phụ lục giao dịch liên kết kèm theo Quyết toán TNDN).

- Compliance with the arm's length principle is required (prices must be within market price range).

- Pay special attention to the interest expense limit.

Interest expense and EBITDA limit

This is one of the most prominent and controversial points of the regulations on related-party transactions in Decree 132/2020/ND-CP:

- Limiting principle: The total interest expense deductible when determining corporate income tax (after deducting interest on deposits and loans) must not exceed 30% of the total net profit from business operations (EBITDA) generated during the period.

Important new points:

- Cho phép chuyển phần chi phí lãi vay không được trừ (phần vượt 30% EBITDA) sang các kỳ tính thuế tiếp theo, tối đa 05 năm.

- The portion of interest expense exceeding the 30% EBITDA limit that is not deductible will be reduced if the business has related-party transactions that are exempt from preparing valuation reports, or only involves related-party borrowing or lending transactions.

Câu hỏi thường gặp về giao dịch liên kết Nghị định 132

Bắt buộc phải kê khai. Ngay cả khi doanh nghiệp chỉ phát sinh giao dịch vay vốn với bên liên kết thì vẫn phải kê khai Phụ lục I, theo dõi giới hạn chi phí lãi vay và chứng minh lãi suất vay phù hợp nguyên tắc giao dịch độc lập.

Phần chi phí lãi vay vượt mức 30% EBITDA không được tính vào chi phí được trừ trong kỳ nhưng được chuyển sang tối đa 05 năm tiếp theo nếu đáp ứng điều kiện. Lưu ý cho doanh nghiệp có tỷ lệ vay vốn nội bộ cao cần đặc biệt theo dõi quy định này để tránh bị truy thu thuế.

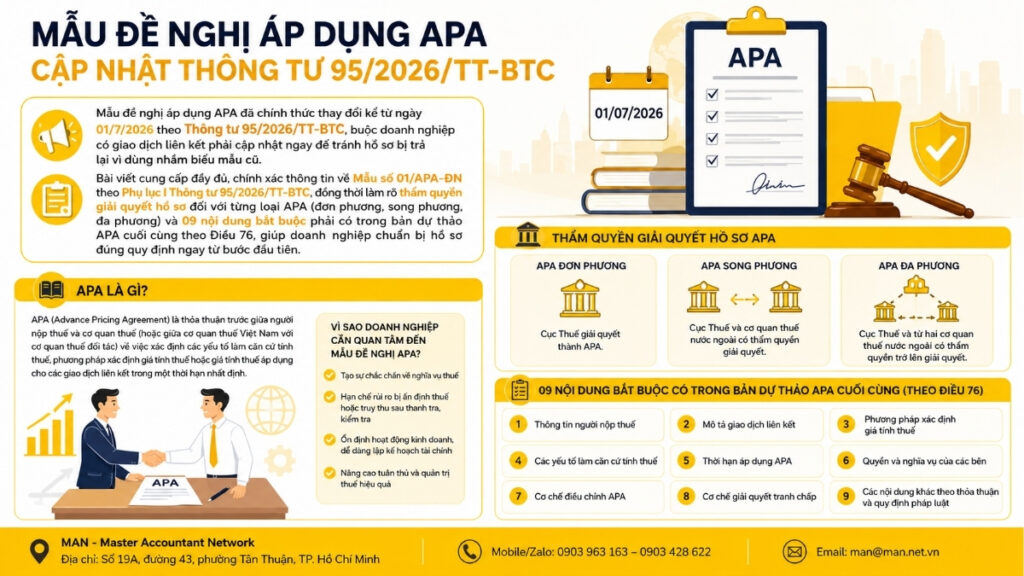

APA (Advance Pricing Agreement) là Thỏa thuận trước về phương pháp xác định giá tính thuế giữa doanh nghiệp và cơ quan thuế. Phương pháp này giúp giảm rủi ro thanh tra, tăng tính chắc chắn về chính sách thuế và hạn chế tranh chấp với cơ quan thuế.

Doanh nghiệp cần lưu giữ Hồ sơ xác định giá giao dịch liên kết theo thời hạn lưu trữ hồ sơ kế toán và hồ sơ thuế theo quy định pháp luật hiện hành. Doanh nghiệp nên lưu đầy đủ dữ liệu so sánh, hợp đồng, chứng từ thanh toán, hồ sơ dịch vụ nội bộ, chính sách giá chuyển nhượng. Tất cả sẽ bảo vệ doanh nghiệp khi giải trình trước cơ quan thuế.Doanh nghiệp chỉ vay vốn công ty mẹ có phải kê khai giao dịch liên kết không?

Chi phí lãi vay bị khống chế như thế nào theo Nghị định 132?

Ký kết thỏa thuận APA trong giao dịch liên kết là gì?

Hồ sơ giao dịch liên kết phải lưu giữ trong bao lâu?

Conclusion and recommendations

Compliance with the regulations on related-party transactions under Decree 132 is a big challenge but also an opportunity for businesses to make their financial activities transparent, strengthen their reputation and minimize legal risks.

To maintain compliance and sustainable risk control, businesses need to implement additional:

- Periodic Review: Establish a quarterly review process for the ownership structure and management to accurately identify Affiliates and eliminate omission risks.

- Hồ sơ xác định giá giao dịch liên kết là bằng chứng pháp lý chứng minh rằng các giao dịch liên kết của doanh nghiệp được thực hiện theo nguyên tắc thị trường độc lập. Trên thực tế, nhiều doanh nghiệp lựa chọn sử dụng dịch vụ lập hồ sơ giao dịch liên kết nhằm đảm bảo tính đầy đủ của Local File, Master File và giảm thiểu rủi ro khi thanh tra thuế.

- Separating Interest Expense: Track net interest expense and monthly EBITDA separately to manage the 30% limit and proactively balance funding.

Contact MAN – Master Accountant Network để được hỗ trợ và tư vấn miễn phí!

Contact information MAN – Master Accountant Network

- Address: No. 19A, Street 43, Tan Thuan Ward, Ho Chi Minh City

- Mobile/Zalo: 0903 963 163 – 0903 428 622

- E-mail: man@man.net.vn

Content production by: Mr. Lê Hoàng Tuyên – Sáng lập viên (Founder) & CEO MAN – Master Accountant Network, Kiểm toán viên CPA Việt Nam với hơn 30 năm kinh nghiệm trong ngành Kế toán, Kiểm toán và Tư vấn Tài chính.