Tư vấn chuyển giá năm 2026 không còn là một thủ tục tuân thủ đơn thuần mà đã trở thành điều kiện cần thiết giúp doanh nghiệp kiểm soát rủi ro giao dịch liên kết trong bối cảnh Nghị định 255/2026/NĐ-CP, văn bản pháp lý mới nhất về quản lý thuế đối với giao dịch liên kết, chính thức thay thế Nghị định 132/2020/NĐ-CP và Nghị định 20/2025/NĐ-CP kể từ ngày 01/7/2026. Đồng thời, sự vận hành của Thuế tối thiểu toàn cầu (Pillar Two) đang làm thay đổi toàn diện cách doanh nghiệp FDI hoạch định thuế. Bài viết này cung cấp góc nhìn chuyên gia về khung pháp lý mới, phân tích tác động đa chiều của Pillar Two và đưa ra chiến lược tư vấn chuyển giá thực chiến, giúp doanh nghiệp chủ động phòng ngừa truy thu, tối ưu nghĩa vụ thuế và vững vàng trước các cuộc thanh tra thuế ngày càng khắt khe.

Overview of legal regulations on related-party transactions in Vietnam

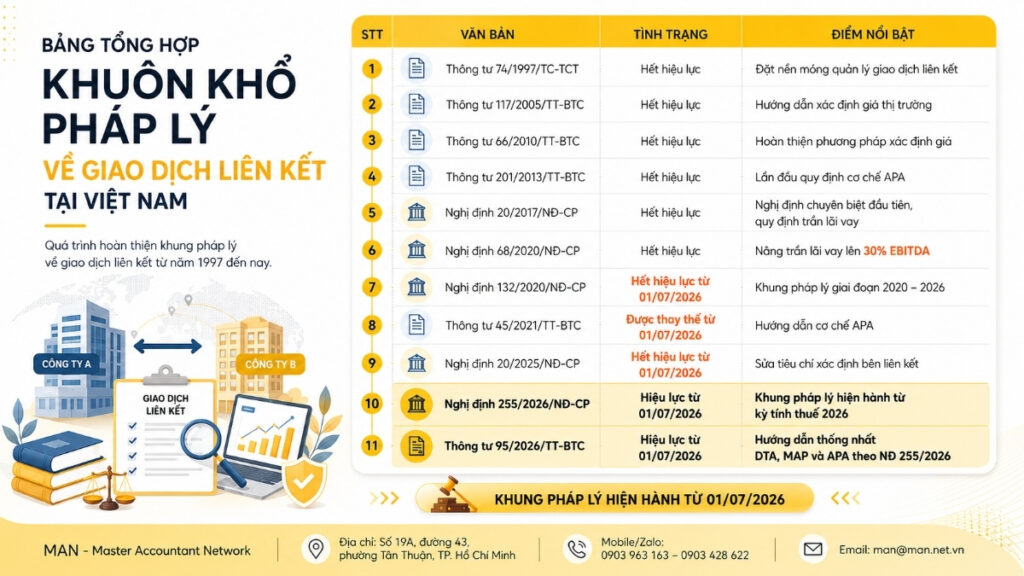

Trong bối cảnh khung pháp lý ngày càng hoàn thiện và siết chặt, việc nắm rõ các quy định cốt lõi về giao dịch liên kết là nền tảng bắt buộc để doanh nghiệp triển khai chiến lược chuyển giá hiệu quả. Kể từ ngày 01/7/2026, trọng tâm pháp lý chuyển sang Nghị định 255/2026/NĐ-CP, văn bản đã hợp nhất và thay thế toàn bộ Nghị định 132/2020/NĐ-CP cùng Nghị định 20/2025/NĐ-CP, đồng thời dẫn chiếu nhiều nội dung tới Luật Quản lý thuế 2025 (Luật số 108/2025/QH15) để bảo đảm tính thống nhất, đồng bộ với hệ thống pháp luật thuế hiện hành.

Nghị định 255/2026/NĐ-CP về giao dịch liên kết (cập nhật thay cho Nghị định 132/2020/NĐ-CP)

Nghị định 255/2026/NĐ-CP (ban hành ngày 30/6/2026, có hiệu lực thi hành từ ngày 01/7/2026 và áp dụng từ kỳ tính thuế thu nhập doanh nghiệp năm 2026) hiện là văn bản pháp lý cao nhất điều chỉnh việc quản lý thuế đối với các giao dịch liên kết của doanh nghiệp có quan hệ liên kết, thay thế Nghị định 132/2020/NĐ-CP và Nghị định 20/2025/NĐ-CP. Việc xác định chính xác các bên liên kết theo Điều 5 Nghị định 255/2026/NĐ-CP vẫn là “nền móng” sống còn của mọi hồ sơ; do đó, doanh nghiệp cần phối hợp chặt chẽ với các đơn vị tư vấn chuyển giá có chuyên môn cao ngay từ bước đầu để nhận diện đúng quan hệ kinh doanh, tránh những sai sót mang tính hệ thống dẫn đến rủi ro ấn định thuế sau này.

Các tiêu chí thường gặp khiến doanh nghiệp rơi vào vòng xoáy giao dịch liên kết về cơ bản vẫn được giữ nguyên như trước đây, bao gồm:

- Sở hữu vốn: One party directly or indirectly holds at least 25% of the other party's equity contribution.

- Mối quan hệ điều hành: Một doanh nghiệp chỉ định thành viên ban điều hành hoặc nắm quyền kiểm soát quyết định tài chính của doanh nghiệp khác.

- Bảo lãnh nợ: Một doanh nghiệp bảo lãnh hoặc cho một doanh nghiệp khác vay vốn dưới bất kỳ hình thức nào ít nhất bằng 25% vốn góp chủ sở hữu và chiếm trên 50% tổng giá trị các khoản nợ trung và dài hạn.

Điểm mới đáng lưu ý tại Điều 5 Nghị định 255/2026/NĐ-CP:

- Bổ sung quan hệ liên kết qua giao dịch mượn, cho mượn: Trước đây, quy định chưa xác định quan hệ liên kết giữa doanh nghiệp với cá nhân điều hành, kiểm soát doanh nghiệp (hoặc cá nhân có quan hệ gia đình liên quan) phát sinh từ việc mượn, cho mượn tài sản. Nghị định 255/2026/NĐ-CP bổ sung: doanh nghiệp có giao dịch vay, cho vay, mượn, cho mượn ít nhất 10% vốn góp của chủ sở hữu tại thời điểm phát sinh giao dịch trong kỳ tính thuế với cá nhân điều hành, kiểm soát doanh nghiệp (hoặc cá nhân thuộc các mối quan hệ liên quan theo quy định) thì được coi là có quan hệ liên kết. Quy định này nhằm khắc phục vướng mắc thực tiễn và phản ánh đúng bản chất giao dịch.

- Bổ sung trường hợp loại trừ quan hệ liên kết đối với bảo lãnh/cho vay từ tổ chức xử lý nợ do Nhà nước sở hữu 100% vốn: Chủ nợ, bên bảo lãnh là tổ chức do Nhà nước sở hữu 100% vốn điều lệ có chức năng mua, bán, xử lý nợ sẽ không bị coi là có quan hệ liên kết với bên nợ hoặc bên được bảo lãnh, nếu tổ chức đó không trực tiếp/gián tiếp điều hành, kiểm soát hoặc góp vốn, đầu tư vào doanh nghiệp bên nợ hoặc được bảo lãnh.

See also: Điểm mới Nghị định 255/2026/NĐ-CP về giao dịch liên kết.

Nguyên tắc áp dụng và nguyên tắc kiểm tra thuế theo Luật Quản lý thuế 2025

The Vietnamese tax authorities have upgraded their audit system based on the principle of "Substance over Form." This means that no matter how tightly worded the contracts between related parties are, if the economic nature of the transaction does not correspond to the profits retained in Vietnam, the company's filing will still be rejected.

Because of this complex technical nature, attempting to handle the documentation yourself or using non-specialized personnel often leads to fatal flaws. Therefore, choosing a qualified professional is crucial. dịch vụ tư vấn giao dịch liên kết Securing the rights of businesses through organizations with extensive experience is a crucial factor in protecting their legitimate interests during rigorous inspections.

Điểm mới đáng lưu ý khác tại Nghị định 255/2026/NĐ-CP:

- Thứ tự ưu tiên sử dụng cơ sở dữ liệu (Điều 17): Nghị định lần đầu quy định thứ tự ưu tiên khi phân tích, so sánh giao dịch liên kết như cơ sở dữ liệu được công bố công khai, cơ sở dữ liệu thương mại, cơ sở dữ liệu của cơ quan thuế. Đồng thời bổ sung cơ sở dữ liệu quốc gia là nguồn dữ liệu tin cậy được sử dụng trong kê khai, xác định, quản lý giá giao dịch liên kết.

- Chuyển dịch từ quản lý rủi ro sang quản lý tuân thủ và hỗ trợ tuân thủ (khoản 10 Điều 21): Cơ quan thuế xây dựng chương trình hỗ trợ người nộp thuế tuân thủ tự nguyện trên cơ sở quản lý rủi ro; công bố tỷ suất lợi nhuận ngành theo lĩnh vực, địa bàn để hỗ trợ doanh nghiệp kê khai, xác định giá giao dịch liên kết theo nguyên tắc giao dịch độc lập; đồng thời có trách nhiệm bảo mật thông tin do người nộp thuế cung cấp khi tham gia chương trình này.

- Không sử dụng Báo cáo lợi nhuận liên quốc gia (CbCR) để điều chỉnh, ấn định giá giao dịch liên kết (điểm c khoản 1 Điều 21): Cơ quan thuế chỉ được quản lý, sử dụng CbCR phục vụ công tác quản lý rủi ro và trao đổi thông tin theo cam kết quốc tế của Việt Nam.

Global Minimum Tax Rate (Pillar Two): A New Variable in Transfer Pricing Advisory

The introduction of the Global Minimum Tax Rate (Pillar Two) not only changed the way taxes are calculated but also reshaped the entire transfer pricing advisory strategy of FDI enterprises. To understand the extent of the impact and develop effective response plans, businesses need to conduct in-depth analysis of each core component, from domestic supplementary tax mechanisms to the direct relationship between transfer pricing and the global effective tax rate.

Resolution 107/2023/QH15 and the pressure on FDI enterprises.

Sự ra đời của Nghị quyết số 107/2023/QH15 (ban hành ngày 29/11/2023 và có hiệu lực thi hành từ ngày 01/01/2024) đã thay đổi hoàn toàn cuộc chơi. Cơ chế Thuế tối thiểu bổ sung nội địa đạt chuẩn (QDMTT) áp dụng cho các tập đoàn có doanh thu hợp nhất toàn cầu từ 750 triệu Euro trở lên, với mức thuế suất hiệu dụng (ETR) tối thiểu phải là 15%. Nghị định 255/2026/NĐ-CP tiếp tục hoàn thiện giải thích từ ngữ “Công ty mẹ tối cao”, “Hiệp định thuế” theo hướng dẫn chiếu tới Nghị quyết 107/2023/QH15 và Nghị định 236/2025/NĐ-CP (hướng dẫn thi hành Nghị quyết này), bảo đảm tính thống nhất giữa quy định về giao dịch liên kết và quy định về thuế tối thiểu toàn cầu.

The dialectical relationship between transfer pricing and Pillar Two

Doanh nghiệp cần sự tư vấn từ các đơn vị chuyên môn để tính toán được điểm cân bằng giữa việc tuân thủ Nghị định 255/2026/NĐ-CP và việc tối ưu hóa nghĩa vụ thuế theo Pillar Two. Liên hệ MAN – Master Accountant Network để được hỗ trợ và tư vấn chuyển giá chi tiết phù hợp cả luật nội địa và các quy tắc GloBE của OECD. Thấu hiểu sự khó khăn của doanh nghiệp khi chính sách thuế luôn thay đổi và cập nhật liên tục, đội ngũ chuyên gia chuyển giá của MAN luôn cập nhật, nghiên cứu để đưa ra giải pháp bảo vệ doanh nghiệp khỏi rủi ro bị đánh thuế trùng hoặc bị phạt do tính toán sai lệch.

Để giúp doanh nghiệp có cái nhìn hệ thống và dễ dàng nhận diện những thay đổi quan trọng nhất kể từ 01/7/2026, dưới đây là bảng so sánh giữa khung pháp lý trước đây (Nghị định 132/2020/NĐ-CP, Nghị định 20/2025/NĐ-CP) và Nghị định 255/2026/NĐ-CP hiện hành.

No longer a matter of individual compliance, businesses are now forced to build a comprehensive strategy, connecting domestic data, consolidated reports, and global tax obligations. This requires businesses to consult highly specialized transfer pricing consultants who are knowledgeable and continuously updated on new tax policies to ensure valid documentation, proactively control risks, optimize profit structure, and be prepared to explain themselves in an increasingly data-driven and risk-based tax audit environment.

| Criteria | Trước 01/7/2026 | Từ 01/7/2026 | Impact |

| Legal basis | Nghị định 132/2020/NĐ-CP là văn bản gốc; Nghị định 20/2025/NĐ-CP sửa đổi, bổ sung một số nội dung. | Nghị định 255/2026/NĐ-CP hợp nhất, thay thế toàn bộ hai văn bản trên; nhiều nội dung dẫn chiếu trực tiếp tới Luật Quản lý thuế 2025 và Nghị quyết 107/2023/QH15. | Doanh nghiệp cần rà soát lại toàn bộ quy trình tuân thủ và tư vấn chuyển giá để đồng bộ với văn bản mới. |

| Quan hệ liên kết qua vay/mượn với cá nhân điều hành | Chưa quy định quan hệ liên kết phát sinh từ việc mượn, cho mượn tài sản. | Bổ sung: Vay, cho vay, mượn, cho mượn từ 10% vốn góp chủ sở hữu trở lên với cá nhân điều hành, kiểm soát doanh nghiệp (hoặc người có quan hệ liên quan) tạo thành quan hệ liên kết. | Doanh nghiệp cần rà soát thêm các giao dịch mượn tài sản với cá nhân quản lý, tránh bỏ sót quan hệ liên kết. |

| Miễn lập Hồ sơ xác định giá giao dịch liên kết | Phải đáp ứng đồng thời 04 tiêu chí: Chức năng kinh doanh đơn giản Không phát sinh doanh thu, chi phí từ tài sản vô hình; Doanh thu dưới 200 tỷ đồng Đạt tỷ suất lợi nhuận thuần tối thiểu theo lĩnh vực. | Nâng ngưỡng doanh thu lên dưới 500 tỷ đồng; bỏ tiêu chí “chức năng kinh doanh đơn giản”; vẫn giữ điều kiện về tỷ suất lợi nhuận thuần tối thiểu theo lĩnh vực. | Mở rộng đối tượng doanh nghiệp rủi ro thấp được miễn lập hồ sơ, giảm chi phí tuân thủ. |

| Control interest costs | Tối a 30% EBITDA; được chuyển chi phí lãi vay vượt mức sang kỳ sau tối đa 5 năm. | Về nguyên tắc vẫn giữ mức trần 30% EBITDA; doanh nghiệp thuộc diện chuyển tiếp theo Điều 3 Nghị định 20/2025/NĐ-CP tiếp tục được áp dụng cho thời gian còn lại theo đúng quy định đó dù văn bản gốc đã hết hiệu lực. | Doanh nghiệp đang trong giai đoạn chuyển tiếp cần lưu giữ hồ sơ chứng minh điều kiện chuyển tiếp để không bị mất quyền lợi. |

| Cơ sở dữ liệu so sánh | Cho phép sử dụng dữ liệu từ phân vị thứ 35 đến 75; chưa quy định thứ tự ưu tiên nguồn dữ liệu. | Bổ sung thứ tự ưu tiên: Dữ liệu công khai; Dữ liệu thương mại Dữ liệu của cơ quan thuế Đồng thời bổ sung cơ sở dữ liệu quốc gia làm nguồn tham chiếu. | Doanh nghiệp cần minh bạch hóa nguồn dữ liệu benchmarking, ưu tiên dữ liệu công khai/thương mại có bản quyền để tránh bị bác bỏ hồ sơ. |

| Country-by-Country Reporting (CbCR) | Ngưỡng doanh thu hợp nhất toàn cầu cố định 18.000 tỷ đồng, căn cứ theo doanh thu trong kỳ tính thuế. | Nâng ngưỡng chuyển sang tương đương 750 triệu Euro, căn cứ theo doanh thu của năm tài chính liền kề trước năm báo cáo, quy đổi theo tỷ giá trung tâm hoặc tỷ giá tính chéo tháng 12 do Ngân hàng Nhà nước công bố; bổ sung Mẫu Thông báo 01/TB-BCLN, chỉ nộp một lần khi phát sinh nghĩa vụ lần đầu; định dạng nộp XML mã hóa qua Hệ thống thông tin quản lý thuế. | Doanh nghiệp thuộc diện lập CbCR cần cập nhật cách xác định ngưỡng doanh thu và quy trình nộp thông báo theo mẫu mới. |

| Sử dụng CbCR trong quản lý thuế | Không sử dụng CbCR để ấn định giá giao dịch liên kết. | Bổ sung rõ: CbCR chỉ phục vụ quản lý rủi ro, trao đổi thông tin theo cam kết quốc tế, không được sử dụng để điều chỉnh hoặc ấn định giá giao dịch liên kết. | Tăng tính minh bạch, bảo vệ quyền lợi người nộp thuế khi cung cấp CbCR. |

| Mô hình quản lý thuế | The explanation is based on the records compiled when an inspection is requested. | Chuyển sang mô hình tự khai, tự tính, tự chịu trách nhiệm kết hợp giám sát dựa trên rủi ro; bổ sung chương trình hỗ trợ tuân thủ tự nguyện (khoản 10 Điều 21). | Tăng vai trò chủ động của doanh nghiệp; đồng thời có thêm kênh hỗ trợ từ cơ quan thuế nếu tham gia chương trình tự nguyện. |

Details of professional transfer pricing consulting services

Để thiết lập một hệ thống phòng thủ thuế vững chắc, doanh nghiệp cần thực thi các hạng mục kỹ thuật chuyên sâu cùng với sự hỗ trợ từ các đơn vị tư vấn giao dịch liên kết tại TPHCM uy tín. Chi tiết các hạng mục bao gồm:

Establish a standardized three-tiered documentation system.

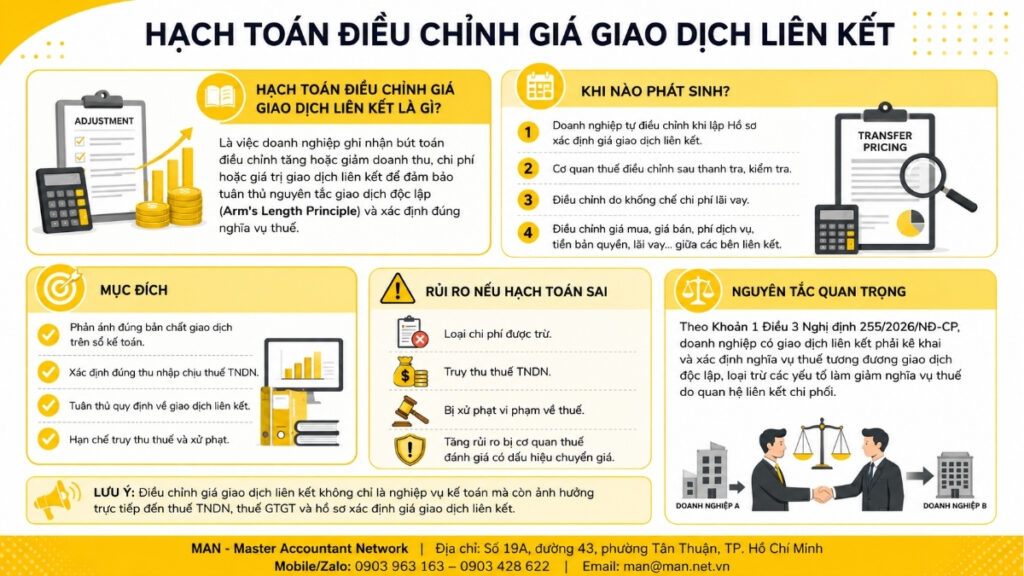

Theo Nghị định 255/2026/NĐ-CP, người nộp thuế có nghĩa vụ kê khai thông tin về quan hệ liên kết và giao dịch liên kết theo Phụ lục I, II, III ban hành kèm theo Nghị định, nộp cùng Tờ khai quyết toán thuế thu nhập doanh nghiệp, cũng như lập, lưu giữ và cung cấp Hồ sơ xác định giá giao dịch liên kết khi được yêu cầu, bao gồm:

- Hồ sơ quốc gia (Local File): Tập trung phân tích chuyên sâu các giao dịch tại thực thể Việt Nam theo danh mục nội dung tại Phụ lục II. Trọng tâm là phần phân tích chức năng, tài sản và rủi ro (FAR Analysis) để chứng minh tính hợp lý của lợi nhuận để lại.

- Hồ sơ toàn cầu (Master File): Cung cấp bức tranh toàn cảnh về chuỗi giá trị, cơ cấu sở hữu trí tuệ và các thỏa thuận tài chính nội bộ của tập đoàn mẹ theo danh mục nội dung tại Phụ lục III, đảm bảo không có sự mâu thuẫn với thông tin tại Việt Nam.

- Báo cáo lợi nhuận liên quốc gia (CbCR): Dành cho các MNEs có doanh thu hợp nhất toàn cầu từ mức tương đương 750 triệu Euro trở lên (theo doanh thu năm tài chính liền kề trước năm báo cáo), lập theo Điều 19 và Phụ lục IV Nghị định 255/2026/NĐ-CP, thể hiện sự minh bạch về việc phân bổ doanh thu và thuế thu nhập tại từng quốc gia có hoạt động kinh doanh.

Quantitative Comparative Analysis (Benchmarking Study)

Đây là công cụ kỹ thuật then chốt để xác định Giá thị trường cho giao dịch liên kết:

- Truy xuất cơ sở dữ liệu theo đúng thứ tự ưu tiên mới: Nghị định 255/2026/NĐ-CP yêu cầu ưu tiên sử dụng, tiếp đến dữ liệu công bố công khai, dữ liệu thương mại từ các nền tảng chuyên nghiệp như Orbis (Bureau van Dijk) hay Moody’s Analytics; và cuối cùng mới đến dữ liệu của cơ quan thuế, đồng thời có thể tham chiếu thêm cơ sở dữ liệu quốc gia mới được bổ sung.

- Sàng lọc đối tượng so sánh: Áp dụng các tiêu chí loại trừ nghiêm ngặt về ngành nghề, thị trường địa lý và tình trạng tài chính (không lỗ lũy kế kéo dài).

- Điều chỉnh khác biệt: Thực hiện các bút toán điều chỉnh kỹ thuật về vốn lưu động, hàng tồn kho, hoặc rủi ro thị trường để đưa các đối tượng so sánh về cùng một mặt bằng tham chiếu với doanh nghiệp.

Periodic Risk Review and Inspection Support

Chủ động nhận diện lỗ hổng trước khi Cơ quan Thuế phát hiện, đồng thời tận dụng cơ chế hỗ trợ tuân thủ mới:

- Rà soát chi phí lãi vay: Kiểm tra tính tuân thủ của mức trần 30% EBITDA; đối với doanh nghiệp thuộc diện chuyển tiếp theo Điều 3 Nghị định 20/2025/NĐ-CP, cần lưu giữ hồ sơ chứng minh điều kiện để tiếp tục được hưởng chuyển tiếp cho thời gian còn lại theo khoản 3 Điều 23 Nghị định 255/2026/NĐ-CP.

- Assessing the reasonableness of internal service fees: Demonstrate that corporate management fees and royalty fees genuinely provide economic benefits to the entity in Vietnam.

- Tham khảo tỷ suất lợi nhuận ngành do cơ quan thuế công bố: Theo quy định mới, cơ quan thuế có trách nhiệm công bố tỷ suất lợi nhuận ngành theo lĩnh vực, địa bàn để hỗ trợ doanh nghiệp tự kê khai, xác định giá giao dịch liên kết theo nguyên tắc giao dịch độc lập; doanh nghiệp có thể tham khảo dữ liệu này khi tự đánh giá rủi ro.

- Develop a justification script: Prepare strong technical arguments to defend your company's profit margin when facing a tax audit team on-site.

Businesses can refer to the details. chi phí lập hồ sơ giao dịch liên kết Visit MAN – Master Accountant Network to create a suitable budget plan.

Losing money and getting nothing in return with overly cheap transfer pricing consulting services.

Đặc biệt trong mùa quyết toán cao điểm, áp lực quyết toán thuế tăng cao, nhiều đơn vị tư vấn kém uy tín, chuyên môn đã nắm bắt thời cơ, thời hạn cận kề. Nhiều đơn vị “ma” đã tung ra các gói dịch vụ giá rẻ để thu hút doanh nghiệp đăng ký sử dụng. Tuy nhiên, việc đánh đổi sự an toàn của tập đoàn lấy một khoản tiết kiệm chi phí tư vấn nhỏ có thể dẫn đến những thảm họa tài chính, đặc biệt trong giai đoạn chuyển tiếp sang Nghị định 255/2026/NĐ-CP khi nhiều quy định mới đòi hỏi cập nhật kịp thời. Cụ thể như sau:

Hồ sơ sao chép và sự thiếu hụt chất lượng chuyên môn

Phần lớn các đơn vị giá rẻ không thực hiện phân tích sâu về đặc thù kinh doanh của doanh nghiệp (Phân tích FAR Analysis). Thay vào đó, họ sử dụng các mẫu hồ sơ có sẵn và chỉ thay đổi tên doanh nghiệp, địa chỉ,…. Điều này khiến hồ sơ thiếu tính thuyết phục và minh bạch, dẫn tới không giải trình được bản chất kinh tế của các giao dịch và dễ dàng bị cơ quan thuế bác bỏ ngay từ vòng soát xét đầu tiên.

The benchmarking data is inaccurate and outdated.

Đơn vị cung cấp dịch vụ tư vấn chuyển giá uy tín và đúng chuẩn sẽ tuân thủ đúng thứ tự ưu tiên cơ sở dữ liệu theo Nghị định 255/2026/NĐ-CP, sử dụng nguồn dữ liệu chất lượng và chuẩn như Orbis, Moody’s…

Đơn vị cung cấp giá rẻ thường sử dụng dữ liệu rác, dữ liệu thu thập không chính thống hoặc dữ liệu cũ đã lỗi thời, không theo đúng thứ tự ưu tiên mà quy định mới yêu cầu. Khi cơ quan thuế sử dụng hệ thống dữ liệu để đối chiếu, sự sai lệch này sẽ là bằng chứng đanh thép để họ thực hiện quyền ấn định thuế.

Thiếu cập nhật về Thuế tối thiểu toàn cầu (Pillar Two) và Nghị định 255/2026/NĐ-CP

Dịch vụ giá rẻ thường chỉ dừng lại ở việc lập hồ sơ địa phương (Local File) cơ bản theo mẫu cũ. Họ hoàn toàn bỏ qua các tác động của Nghị quyết 107/2023/QH15 cũng như các điểm mới của Nghị định 255/2026/NĐ-CP như quan hệ liên kết qua mượn – cho mượn, ngưỡng miễn lập hồ sơ mới, hay ngưỡng CbCR theo chuẩn 750 triệu Euro. Nếu hồ sơ chuyển giá không đồng nhất với báo cáo Pillar Two của tập đoàn mẹ hoặc không cập nhật quy định mới, doanh nghiệp sẽ đối mặt với rủi ro bị truy thu thuế bổ sung tại cả Việt Nam và quốc gia của công ty mẹ.

Bỏ rơi khách hàng trong giai đoạn giải trình thanh tra

The most serious consequence of using unreliable services is the lack of accountability when tax inspectors intervene. These agencies lack the expertise to argue with the inspection team, leaving businesses to face tax collection and late payment penalties amounting to tens of billions of dong alone. A poor-quality transfer pricing consulting report is the "shortest path" to having profits artificially assessed.

Why is MAN – Master Accountant Network a trusted partner?

Giữa muôn vàn đơn vị cung cấp dịch vụ, MAN – Master Accountant Network khẳng định vị thế thông qua việc cung cấp giải pháp tư vấn chuyển giá toàn diện, kết hợp giữa kinh nghiệm thực chiến, nền tảng công nghệ dữ liệu hiện đại và khả năng cập nhật liên tục các quy định mới như Nghị định 255/2026/NĐ-CP.

A team of highly qualified experts

At MAN, we have a team of experts with over 30 years of experience in the field of Taxation and Finance. This team includes not only Certified Public Accountants (CPAs) but also internationally certified professionals (ACCA) with in-depth knowledge of Vietnamese tax law as well as OECD international practices. This gives MAN a multifaceted perspective, combining technical data analysis with solid legal arguments.

Access to the international copyright database

MAN đầu tư mỗi năm để duy trì quyền truy cập vào các hệ thống dữ liệu doanh nghiệp toàn cầu (như Orbis, Moody’s Analytics), phù hợp với thứ tự ưu tiên dữ liệu mới theo Nghị định 255/2026/NĐ-CP. Đây là dữ liệu quan trọng nhất để thực hiện Phân tích so sánh (Benchmarking) đạt chuẩn, đảm bảo rằng các đối tượng so sánh độc lập được lựa chọn luôn có độ tin cậy cao nhất và khó bị bác bỏ bởi Cơ quan Thuế.

Commitment to support throughout the inspection process.

MAN – Master Accountant Network is committed to supporting businesses from the planning and documentation stages to directly participating in explanations before inspection teams. We represent businesses to defend economic and technical arguments, ensuring that the risk of tax assessment is always kept to a minimum.

Conclude

Đừng để những sai sót nhỏ hoặc sự lựa chọn đơn vị tư vấn sai lầm phá hủy thành quả kinh doanh của tập đoàn. Contact MAN – Master Accountant Network để được tư vấn chuyển giá và hỗ trợ đưa ra chiến lược thuế cho những năm tiếp theo!

Contact information MAN – Master Accountant Network

- Address: Số 19A, Đường 43, Phường Tân Thuận, TP. Hồ Chí Minh

- Mobile/Zalo: 0903 963 163 – 0903 428 622

- E-mail: man@man.net.vn

- Google Business Profile: Xem Google Business Profile của MAN – Master Accountant Network

- LinkedIn Founder: Xem hồ sơ LinkedIn của chuyên gia Lê Hoàng Tuyên

Phụ trách sản xuất và kiểm duyệt nội dung chuyên môn bởi: Ông Lê Hoàng Tuyên – Sáng lập viên (Founder) & CEO MAN – Master Accountant Network. Ông là Kiểm toán viên CPA Việt Nam với hơn 30 năm kinh nghiệm sâu sắc trong lĩnh vực Kế toán, Kiểm toán, Thuế và Tư vấn Pháp lý doanh nghiệp.

Câu hỏi thường gặp về tư vấn chuyển giá

Tiêu chí xác định bên liên kết theo Nghị định 255/2026/NĐ-CP có gì thay đổi không?

Về cơ bản, các tiêu chí cốt lõi như sở hữu vốn, quyền điều hành hoặc bảo lãnh nợ vẫn được giữ nguyên. Tuy nhiên, Nghị định 255/2026/NĐ-CP bổ sung quan hệ liên kết phát sinh từ giao dịch mượn, cho mượn từ 10% vốn góp trở lên với cá nhân điều hành, kiểm soát doanh nghiệp, đồng thời bổ sung trường hợp loại trừ đối với chủ nợ/bên bảo lãnh là tổ chức xử lý nợ do Nhà nước sở hữu 100% vốn không tham gia điều hành, kiểm soát doanh nghiệp bên nợ.

Làm thế nào để chứng minh phí dịch vụ nội bộ tập đoàn là hợp lệ?

Để được khấu trừ, doanh nghiệp phải chứng minh dịch vụ mang lại lợi ích kinh tế trực tiếp và mức phí tuân thủ nguyên tắc giá thị trường. Hồ sơ cần cung cấp bằng chứng về việc cung cấp dịch vụ thực tế, phương pháp phân bổ chi phí minh bạch và thực hiện phân tích FAR (Chức năng, Tài sản, Rủi ro) theo danh mục thông tin, tài liệu quy định tại Phụ lục II Nghị định 255/2026/NĐ-CP để bảo vệ tính hợp lý.

Doanh nghiệp nào được miễn lập Hồ sơ xác định giá giao dịch liên kết theo Nghị định 255/2026/NĐ-CP?

Thuế tối thiểu toàn cầu ảnh hưởng thế nào đến chiến lược chuyển giá của MNEs?

Thuế tối thiểu toàn cầu (Pillar Two) tạo ra mức thuế hiệu dụng tối thiểu 15%, làm giảm động lực chuyển lợi nhuận sang các quốc gia thuế suất thấp. Doanh nghiệp cần phối hợp giữa hồ sơ chuyển giá (Local File) theo Nghị định 255/2026/NĐ-CP và báo cáo QDMTT để đảm bảo lợi nhuận phân bổ tại Việt Nam tương xứng với hoạt động thực tế, tránh việc bị đánh thuế bổ sung ở cả hai quốc gia.