In the economic landscape of 2026, managing cash flow and complying with tax regulations will become crucial for every business. One common question many chief accountants and business owners ask is: Does borrowing money from the CEO constitute a related-party transaction?

In fact, many businesses borrow funds from their directors to supplement working capital. However, if the nature of this transaction is misidentified, the business may face the risk of being assessed for tax, having interest expense disallowed, or being subject to retroactive personal income tax collection.

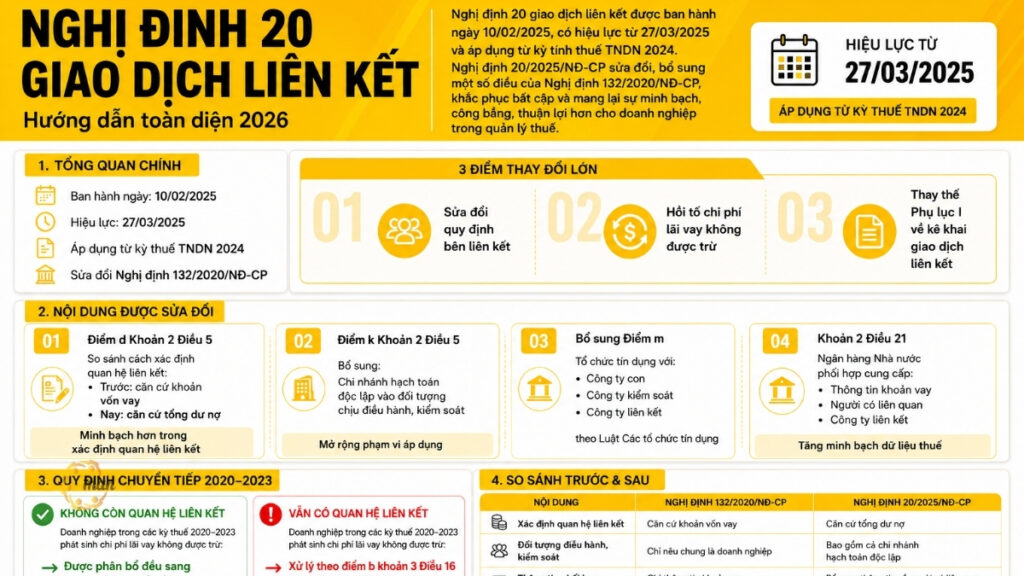

The article below will provide a detailed analysis based on legal regulations. Decree 132/2020/ND-CP and Decree 20/2025/ND-CP Amendments and additions from Decree 132.

The reality of internal borrowing and the pressure of tax audits.

In Vietnam, particularly among small and medium-sized enterprises (SMEs), it is extremely common for directors or executives to lend money to their companies to supplement working capital. However, since 2024, tax authorities have strengthened and tightened control over these cash flows, integrating bank data to closely monitor them.

Therefore, the question of whether borrowing money from a director constitutes a related-party transaction is no longer a theoretical issue but has become a central focus in many tax audits.

If the business identifies it incorrectly:

- Interest expenses may be excluded from deductible expenses.

- The interest rate for 0% may be determined by the tax authorities based on market rates.

- Tax arrears and late payment penalties may arise.

Is borrowing money from a director considered a related-party transaction?

For a loan between an individual director and a business to be considered a related-party transaction, two conditions must be met simultaneously: the relationship between the director and the resulting transaction.

Conditions regarding the relationship

According to Clause 2, Article 5 of Decree 132/2020/ND-CP, two parties are considered to have an affiliated relationship if:

“One or more individuals, as defined in point g of this clause, through their capital contribution to another enterprise or by directly managing or controlling that enterprise…”

More specifically, the Director is the person directly in charge of running and managing the business. Therefore, there is always an inherent managerial relationship between the Director and the company.

Conditions regarding transaction value threshold

This is the key point in answering the question of whether borrowing money from a director constitutes a related-party transaction. Not every loan automatically constitutes a related-party transaction; the value threshold must be considered.

- If a business borrows money from its executive (Director) and that loan is at least equal to 10% of the owner's equity.

- Determination time: At the time the transaction occurs during the tax period.

For example: Company X has a registered capital (paid-up capital) of 5 billion VND. In 2026, the Director lent the company 600 million VND to purchase machinery.

- The loan-to-value ratio was then 12%

- According to Decree 132/2020/ND-CP, if the loan is at least equal to 10% of the owner's equity, then a related-party relationship is established. In this case, it is 12%, so Company X and its Director have a related-party relationship as defined by law.

Interest-free loan cases (Interest rate 0%)

Many accountants mistakenly believe that if a loan is made without interest, it's not considered a business transaction and therefore nothing to worry about. This is a fatal mistake. The law stipulates that related-party transactions include lending assets and money without incurring costs. Therefore, whether a director's loan constitutes a related-party transaction doesn't depend on whether or not there's interest, but rather on the loan-to-equity ratio.

Tax implications of related-party transactions in 2026

Once it has been determined that borrowing money from the director constitutes a related-party transaction, the business faces three major challenges:

Controlling interest expense (30% EBITDA)

According to Article 15 of Decree 132, the total interest expense deductible when determining corporate income tax must not exceed 30% of the total net profit from business operations plus interest expense and depreciation expense (EBITDA).

- If EBITDA is negative: All interest expense for the period will be disallowed.

- The portion of interest expense exceeding the 30% ceiling: Can be carried forward to the next tax period if the business generates profit, for a period not exceeding 5 years.

See details: Formula for calculating interest on related-party transactions.

Risk of being taxed

In related-party transactions, the price (interest rate) must comply with the Arm's Length Principle. If the Director lends at an interest rate of 0% or an interest rate that is excessively high compared to banks, the tax authorities have the right to:

- Setting the input interest rate: Based on the average interest rate of commercial banks at the same time. This creates fictitious interest expense, but it is capped by the 30% EBITDA ceiling.

- Personal Income Tax Collection: If the loan has interest, the Director must pay 5% personal income tax on the capital investment. If the interest rate is 0%, the tax authority may determine the Director's personal income and require tax payment.

Obligation to declare related-party transactions

Businesses must prepare and submit Appendices (I, II, III, IV) along with the corporate income tax return. In particular, according to updates from Decree 20/2025/ND-CP, the forms have been simplified for SMEs, but the requirements for data accuracy are higher.

See details: Instructions for declaring related-party transactions.

Key new points to note in Decree 20/2025/ND-CP

According to Decree 20/2025/ND-CP amending and supplementing Clause 2, Article 5 of Decree 132/2020/ND-CP, the criteria for identifying affiliated parties are as follows:

When are bank loans not considered related-party transactions?

The new regulations retain the criteria for determining the relationship between the borrower and the lender, whereby a loan is considered to have a related party element when the loan value from one party reaches 251 TP3T of the company's equity or more and simultaneously accounts for over 501 TP3T of the company's total medium and long-term debt. This threshold was previously stipulated in Decree 132/2020/ND-CP.

However, the amended regulations have added several important exceptions to exclude credit relationships of a purely commercial nature. Specifically, the above criterion will not apply if the lender or guarantor is a credit institution operating under the Law on Credit Institutions, provided that this institution does not participate in the management, control, capital contribution, or investment in the borrowing enterprise. In addition, the borrowing enterprise must not fall under any other related-party arrangements as stipulated in Clause 2, Article 5.

Furthermore, the regulations clarify that if a credit institution acts as a lender or guarantor, but there is no other related-party relationship between the bank and the borrowing enterprise according to the criteria specified in points b, e… of Clause 2, Article 5, then this loan will not be considered to have arisen from a related-party relationship.

According to regulations effective from March 27, 2025, certain cases of borrowing from banks will no longer be subject to the criteria in point d, clause 2, Article 5 of Decree 132/2020/ND-CP. This means that, even if the loan from the bank reaches or exceeds 25% of equity capital and simultaneously accounts for over 50% of total medium and long-term outstanding debt, the enterprise will still not be considered to have an affiliated relationship if it meets one of the following two conditions:

- The bank does not directly or indirectly participate in the management, control, capital contribution, or investment of the borrowing enterprise.

- The relationship between banks and borrowing businesses does not involve control or influence from a third party; that is, no single organization or individual simultaneously controls both parties.

These adjustments help to clearly distinguish between ordinary commercial credit relationships and related-party relationships with controlling elements, thereby reducing the obligation to declare related-party transactions for businesses in cases of purely bank loans. At the same time, the new regulations also ensure that the determination of related-party relationships accurately reflects the actual controlling nature and power of the parties involved.

The relationship is based on actual power and control.

Point k, Clause 2, Article 5 of Decree No. 132/2020/ND-CP is amended as follows:

“"Other cases in which a business (including independently accounting branches that declare and pay corporate income tax) is subject to the actual management, control, and decision-making power over the business operations of another business."”

Strengthening the linkages between credit institutions and businesses within the same system.

Point m, Clause 2, Article 5 of Decree No. 132/2020/ND-CP is amended as follows:

“Credit institutions with Subsidiaries or with Controlling Companies or with Affiliated Companies of credit institutions as prescribed in the Law on Credit Institutions and amendments, supplements or replacements (if any)”

Deadline for submitting Transfer Pricing Documents

One of the most important issues, especially during the peak tax filing period, is the deadline for submitting documents. Specifically, the Local File and Master File are two core documents that businesses need to prepare and provide as required by regulations when requested by the tax authorities.

Deadline for submitting National and Global Applications

This is a common misunderstanding among businesses when fulfilling their obligations regarding documentation for determining transfer pricing. Unlike the related-party transaction appendices that must be submitted with the corporate income tax return, the Local File and Master File are not required to be submitted at the same time as the tax return.

However, businesses must still prepare and maintain records at their premises before filing their tax returns, so that they can provide them immediately upon request from the tax authorities.

When the tax authorities conduct a tax audit or inspection, businesses must provide documents within the following timeframes:

Pre-inspection consultation phase

Businesses must provide the documents within a maximum of 30 working days from the date of receiving the request from the tax authority.

On-site inspection phase

The deadline for submitting documents is usually no more than 15 working days from the date the inspection team requests them, or as specified in the inspection decision.

Cases eligible for extension

- Businesses may request a one-time extension for submitting documents if there is a valid reason.

- Maximum extension period: 15 working days.

- Extensions will only be granted if the tax authorities give their written consent.

Legal risks and specific penalties businesses need to know.

When related-party transactions occur without proper procedures, businesses will face a barrage of fines. Decree 125/2020/ND-CP and the Tax Administration Law.

Penalties for violations of declaration procedures.

If a business incorrectly determines whether a loan taken out by a director constitutes a related-party transaction, and consequently fails to submit the relevant related-party transaction appendices:

- Fines ranging from 8,000,000 to 15,000,000 VND: For filing tax returns more than 31 to 90 days after the deadline.

- A fine of 15,000,000 to 25,000,000 VND will be imposed for submitting tax returns more than 90 days after the deadline without incurring any additional tax liability.

- Failure to submit the Appendix: The tax authorities have the right to directly assess the tax due to incomplete tax return documentation.

"Tax assessment risk" and types of expenses

This is the biggest financial risk when incorrectly answering the question of whether borrowing money from a director constitutes a related-party transaction:

- Type of interest expense exceeding the 30% EBITDA ceiling: If EBITDA is low or negative, the entire portion of interest expense paid to directors (even if real) will be disallowed as a deductible expense when calculating corporate income tax. The business will be subject to retroactive corporate income tax collection on this disallowed expense.

- Setting interest rates for loans/rentals: If a business lends money (0%), the tax authorities will set an interest rate (usually 7-9%/year depending on the time). The business will be subject to retroactive corporate income tax collection on the additional financial revenue that is assessed.

Penalties for tax violations:

- Penalty 20% on the additional tax amount to be collected (due to incorrect declaration resulting in underpayment of tax).

- Late payment penalty: Calculated at 0.031 TP3T/day on the amount of tax overdue. For audit periods lasting 3-5 years, this amount can reach 40-501 TP3T of the original tax amount.

Risks to the Director personally

Personal income tax on capital investment: If the loan generates interest, the Director must pay 5% personal income tax. Failure to declare will incur late payment penalties and penalties for incorrect declarations, similar to those applied to businesses.

To mitigate risks, especially during peak periods, businesses should consider the following: transfer pricing services or Transfer pricing consultancy To receive support from our affiliate trading experts!

5-Step Checklist for Accounting Processes

To effectively manage the risks associated with a director's borrowing and related-party transactions, accountants need to follow a five-step process:

- Balance review: Monthly/quarterly, compare the Director's personal loan balance with the actual contributed charter capital as stated in the Business Registration Certificate.

- Legal verification: Complete the loan agreement and the minutes of the Board of Members/Board of Directors meeting approving the loan (this is crucial to demonstrate objectivity).

- EBITDA calculation: Forecasting deductible interest expenses to adjust financial plans.

- Accurate declaration: Use the latest version of the HTKK software to fill out the Appendix on related-party transactions. Note that the Director's tax identification number must be accurate.

- Record keeping: Records of transfer pricing include Local Files and Master File) needs to be prepared in advance if the business is not exempt from the requirement to establish a business registration.

The optimal way to handle a situation where a director borrows money from a related-party transaction.

To minimize the risks when borrowing money, should the director engage in related-party transactions?

- Increase charter capital: If the business truly needs long-term capital, proceed with increasing charter capital. When equity increases, the 10% threshold will be higher, preventing the loan from falling under the scope of related-party transactions.

- Using the Advance Payment Account (Account 141): For short-term expenses or loans (a few days), these can be processed through advance payment or expense reimbursement transactions. However, this should not be abused as tax inspectors will examine the nature of the cash flow.

- Appropriate interest rate: Instead of a 0% interest rate, set a suitable interest rate (usually equal to or slightly lower than the bank interest rate) and pay the full 5% personal income tax. This demonstrates transparency and avoids being assigned an unfavorable interest rate.

- Closely monitor EBITDA: If the business is in the investment phase and experiencing sustained losses (negative EBITDA), consider alternative financing options or converting the loan into equity.

Conclude

It can be seen that determining whether a loan from a director constitutes a related-party transaction depends not only on the nature of the loan itself, but also on evaluating the related-party relationship and the ratio of the loan value to equity as stipulated by tax laws. If the loan meets the relationship requirements and exceeds the prescribed threshold, the enterprise is required to declare the related-party transaction, control interest expense, and prepare complete documentation for price determination.

In the context of increasing scrutiny of financial data and related-party transactions by tax authorities, understanding the true nature of whether a loan from a director constitutes a related-party transaction will help businesses proactively manage tax risks and avoid unnecessary imposition of interest rates, expense deductions, or tax arrears.

Therefore, businesses need to regularly review internal loans, standardize legal documents, and declare them correctly to ensure compliance with the law and optimize financial operations in a transparent and sustainable manner.

Contact MAN – Master Accountant Network for timely advice and support!

Contact information MAN – Master Accountant Network

- Address: No. 19A, Street 43, Tan Thuan Ward, Ho Chi Minh City

- Mobile/Zalo: 0903 963 163 – 0903 428 622

- E-mail: man@man.net.vn

Content production by: Mr. Le Hoang Tuyen – Founder & CEO MAN – Master Accountant Network, Vietnamese CPA Auditor with over 30 years of experience in Accounting, Auditing and Financial Consulting.

Data source:

- Decree 132/2020/ND-CP

- Decree 20/2025/ND-CP.