Transfer pricing services in District 1 – Reliable and professional.

Transfer pricing services in District 1 are a necessary solution for businesses…

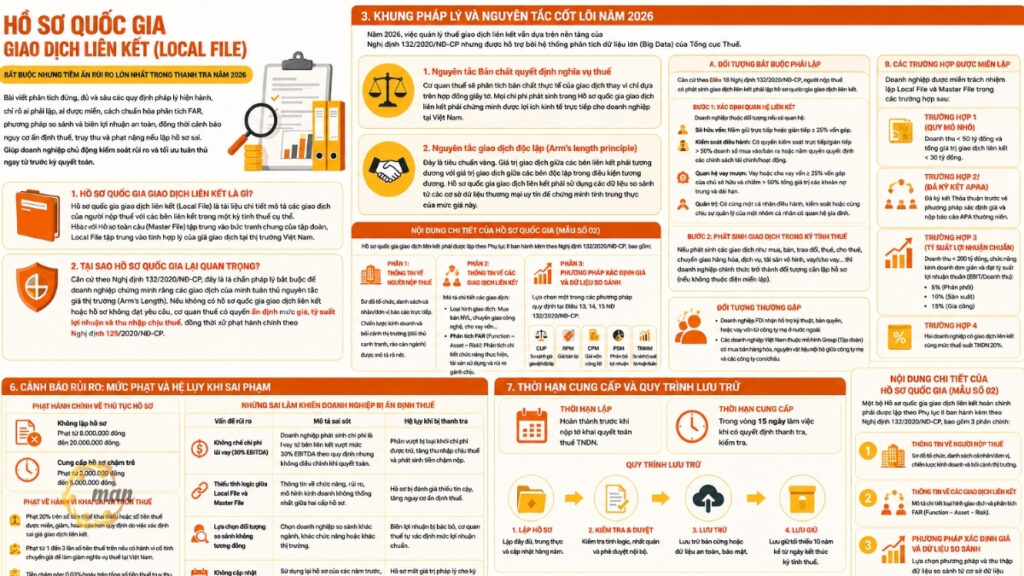

Hồ sơ quốc gia giao dịch liên kết đầy đủ, đúng Nghị định 132

The Local File (or Country File) for related-party transactions is a mandatory document…

Hồ sơ giao dịch liên kết đầy đủ, đúng Nghị định 132

Hồ sơ giao dịch liên kết đang trở thành một trong những nội dung tuân…

The impact of interest expense limits – Why are many businesses being subject to back taxes?

The issue of the impact of controlled interest expense is becoming a major concern…

Non-deductible interest expense and the risk of tax assessment during tax settlement.

Amidst stricter tax audits of related-party transactions, the amount…

Interest expense is deductible – but easily disallowed during audits.

The deductibility of interest expense in related-party transactions is always a matter of concern…