The deadline for submitting related-party transaction documents is one of the important obligations that businesses with related-party transactions must pay special attention to during the tax settlement period. In the context of tax authorities strengthening transfer pricing management through electronic data systems and risk analysis, late submission or incomplete documentation can lead to tax arrears, profit assessment, and many serious legal consequences. This article will analyze in detail the submission deadline, required documents, and risks that businesses need to avoid in 2026.

Understanding Transfer Pricing Documentation Correctly

Before delving into the deadline for submitting related-party transaction documents, businesses need to clearly identify the subjects and components of the documents as stipulated in Decree 132/2020/ND-CP and Decree 20/2025/ND-CP amending and supplementing Decree 132/2020/ND-CP.

What is affiliate trading?

According to Article 5 of Decree 132/2020/ND-CP, related-party transactions are transactions arising between related parties in the production and business process: buying, selling, exchanging, leasing, renting, borrowing, lending, transferring, assigning goods, assets, providing services; borrowing, lending, financial services, financial guarantees and other financial instruments.

The relationship is typically defined by criteria such as capital (e.g., one party directly or indirectly holding at least 25% of the other party's capital contribution) or actual control.

See details: Criteria for determining affiliated relationships

Complete set of application documents

A standard related-party transaction record is not just a few forms, but a data system that includes:

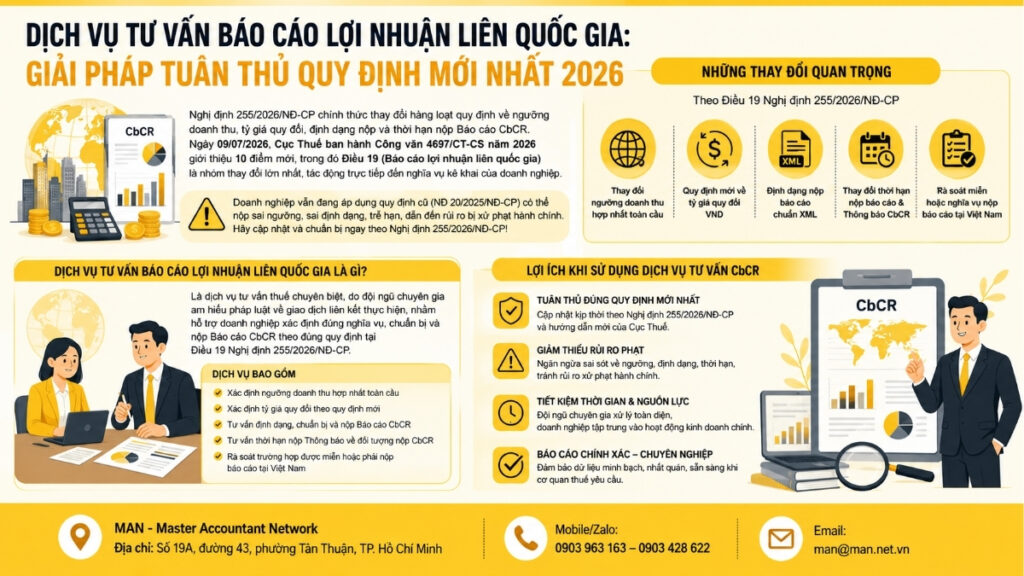

- The attached declarations include Form 01 (Information on related party relationships and related party transactions), Form 02 (List of information and documents in the national file), Form 03 (List of information and documents in the global file), and Form 04 (Country-based profit report).

Transfer pricing documentation (Three-tier documentation):

- Local File: Focuses on specific transactions of entities in Vietnam.

- Master File: Provides an overview of the group's global business structure and transfer pricing policies.

- Country-by-Country Report (CbCR): Details the allocation of income, taxes, and economic indicators of the corporation across each country.

Details of the deadline for submitting related-party transaction documents.

To avoid unfortunate risks, businesses need to pay close attention to the following deadlines for submitting related-party transaction documents:

According to regulations, these appendices are an integral part of the Corporate Income Tax Return. Therefore, the deadline for submitting related-party transaction documents for these appendices coincides with the deadline for submitting the annual Corporate Income Tax Return.

- For businesses whose fiscal year coincides with the calendar year: The deadline is the last day of the third month following the end of the calendar year. Specifically, for the 2025 tax year, businesses must complete the submission of these appendices no later than March 31, 2026.

- For businesses with a fiscal year different from the calendar year: The deadline is the last day of the third month from the end of the fiscal year. For example: If the fiscal year ends on March 31, 2026, the deadline will be June 30, 2026.

Submission method: Submission through the electronic tax system is mandatory, and it is necessary to ensure that the digital signature is valid and that the internet connection is stable during the peak days at the end of March.

Deadline for preparing and submitting the Valuation Documents (Local File and Master File)

This is a point where many businesses frequently get confused. Unlike appendices, the National File and the Global File do not need to be submitted at the same time as the tax return, but must be prepared and stored at the business before the tax return is filed.

Deadline for submission upon request: When tax authorities conduct an audit or inspection, businesses must provide these documents within strict timeframes:

- During the pre-inspection consultation phase: The deadline for providing information is usually no more than 30 working days from the date of receipt of the request.

- During the on-site inspection phase: The timeframe may be shortened to 15 working days or as decided by the inspection team.

Note regarding renewal: Businesses may request an extension for submitting documents once, for a maximum of 15 working days, if there is a force majeure reason or a valid and acceptable reason.

Deadline for submitting the Country-by-Country Report (CbCR)

The CbCR report has more specific regulations regarding the subjects and timeframe:

- Target audience: Ultimate parent companies in Vietnam with consolidated global revenue of VND 18 trillion or more.

- Deadline: No later than 12 months after the end of the fiscal year of the ultimate parent company.

- In the case of a subsidiary in Vietnam: If the ultimate parent company is located abroad in a country with an automatic information exchange agreement with Vietnam, the business in Vietnam does not have to submit directly but must notify the tax authorities about the entity submitting this report globally.

Cases exempt from filing

Understanding the exemptions helps businesses reduce the burden of compliance while still ensuring legal compliance. However, "exemption from filing" does not mean that businesses are outside the scope of transfer pricing controls.

Exemption thresholds for preparing price determination documents.

Businesses are exempt from preparing the Country Profile, Global Profile, and Country-by-Country Report if they fall under one of the following categories:

- The business only conducts transactions with related parties that are subject to corporate income tax in Vietnam, applying the same tax rate, and neither party is entitled to tax incentives.

- Revenue is less than VND 50 billion and the total value of related-party transactions is less than VND 30 billion during the tax period.

- The company has signed an Advance Pricing Agreement (APA) and submits annual APA reports.

- Businesses that perform simple business functions, do not generate revenue or expenses from the exploitation or use of intangible assets, have revenue under VND 200 billion, and achieve a return on sales (ROS) within the prescribed threshold (Distribution: from 51% of 3-year contracts or more; Manufacturing: from 10% of 3-year contracts or more; Processing: from 15% of 3-year contracts or more).

Burden of Proof

Even if exempt from filing transfer pricing documentation, businesses are still required to declare Appendix 01. More importantly, if the tax authorities suspect transfer pricing that results in revenue loss, businesses are still responsible for explaining and providing relevant documents to prove the objectivity of independent transaction prices (Arm's Length Principle).

Legal consequences and financial losses from violations.

Stricter tax management in 2026 means that violations of the deadline for submitting related-party transaction documents will lead to cascading consequences.

Administrative penalties for late payment

Based on Decree 125/2020/ND-CP, the penalty for late submission of tax declaration documents (including related-party transaction appendices) is calculated based on the length of the delay:

- Late payment from 1 to 30 days: Fine from 2 to 5 million VND.

- Late payment from 31 to 60 days: Fine of 5 to 8 million VND.

- Late payment exceeding 90 days: The penalty can be up to 25 million VND.

The power to determine taxes – a "nightmare" for businesses.

This is the most serious risk. If a business fails to comply with the deadline for submitting related-party transaction documents, or submits incomplete documents, or fails to prove the objectivity of the transaction prices, the tax authorities have the right to:

- Eliminate invalid expenses: Particularly interest expenses exceeding 30% EBITDA or internal corporate service expenses that cannot demonstrate economic benefit.

- Setting a profit margin: The tax authorities will use their database to set a "safe zone" for profit. If the company's actual profit margin is lower than the set level, the company must pay additional corporate income tax on the difference.

- Tax arrears and late payment penalties: The tax arrears will be accompanied by a late payment penalty of 0.031 TP3T/day. With audit periods lasting 3-5 years, this amount can increase dramatically.

Loss of tax benefits

Many FDI enterprises are currently enjoying tax incentives (tax exemptions of 2 and reductions of 4, or preferential tax rates of 10%). However, according to regulations, violations of tax management regulations regarding related-party transactions may result in the forfeiture of the right to tax incentives for that tax period.

Reputation repercussions and future audit risks.

When a company violates the deadline for submitting related-party transaction documents, its name will appear with a negative score on the tax authority's risk management system. This leads to:

- Subject to more frequent inspections (possibly annually).

- Facing difficulties in carrying out tax refund or tax settlement procedures for dissolution or merger.

- Loss of credibility when preparing bids for large projects or when working with international financial institutions.

Warning about "Cheap Transfer Pricing Services" and Solutions from MAN

During peak tax filing season, many businesses, under time pressure, seek out cheap transfer pricing consulting services. This is a highly risky option because:

- Inaccurate benchmarking data: Inexperienced firms often select benchmarks that are dissimilar in terms of function, assets, and risk (FAR analysis). When the tax authorities reject the benchmarking data, the company's records are considered invalid.

- Practical experience: Handling complex related-party transactions requires a deep understanding of local industry specifics and global tax policies such as BEPS and OECD Pillar Two. It demands a thorough understanding to connect Vietnam's Decree 132/2020/ND-CP with international tax policies regulating related-party transactions.

MAN - Master Accountant Network - A trusted partner

With over three decades of experience, MAN – Master Accountant Network has established itself as an expert in handling related-party transactions for thousands of FDI enterprises and multinational corporations in Vietnam.

What sets MAN – Master Accountant Network apart is:

- Accurate comparative data: MAN owns and utilizes specialized data sources, ensuring that the comparisons are perfectly aligned with the actual business activities of the company in Vietnam.

- Our team of seasoned experts possesses in-depth knowledge of tax authority procedures, helping businesses develop the most robust price protection strategies.

- Confidentiality and professionalism: We are committed to supporting businesses throughout the entire inspection and on-site audit process, going beyond just preparing documentation.

- Stay up-to-date on new tax policies regulating related-party transactions. Have a thorough understanding of specific tax regulations for related-party transactions, such as the OECD's Global Minimum Tax Rate (Pillar Two), along with Decree 132/2020/ND-CP and Decree 20/2025/ND-CP in Vietnam.

Conclude

Complying with the 2026 deadline for filing related-party transaction reports is not only a legal requirement but also a crucial factor in helping businesses minimize transfer pricing audit risks and protect legitimate expenses during tax settlement. In the context of tax authorities increasingly scrutinizing data and controlling related-party transactions, preparing complete Local File, Master File, and related-party declaration appendices on time will help businesses proactively address any audit situation.

If your business needs to assess transfer pricing risks, prepare related-party transaction documentation, or prepare explanatory documents for tax authorities, please refer to our services. specialized transfer pricing services From MAN. Our team of experts will assist businesses in building proper documentation, ensuring compliance with regulations, and minimizing the risk of tax arrears and tax assessments.

Contact information MAN – Master Accountant Network

- Address: No. 19A, Street 43, Tan Thuan Ward, Ho Chi Minh City

- Mobile/Zalo: 0903 963 163 – 0903 428 622

- E-mail: man@man.net.vn

Content production by: Mr. Le Hoang Tuyen – Founder & CEO MAN – Master Accountant Network, Vietnamese CPA Auditor with over 30 years of experience in Accounting, Auditing and Financial Consulting.

Frequently Asked Questions about the Deadline for Submitting Related Party Transaction Documents

What is the deadline for submitting related-party transaction documents in 2026?

The deadline for submitting related-party transaction documents for the declaration appendices (Forms 01, 02, 03, 04) is the same as the deadline for submitting the corporate income tax return. For businesses whose fiscal year coincides with the calendar year, the deadline is March 31, 2026, for the 2025 tax year. If the business has a fiscal year different from the calendar year, the deadline will be the last day of the third month from the end of the fiscal year.

Do related-party transaction records need to be submitted along with the tax return?

Not entirely. Businesses only need to submit the appendices declaring related-party transactions (Form 01-04) along with the corporate income tax return. For the Local File and Master File, businesses must prepare and store them at their company before submitting the tax return, and only provide them to the tax authorities upon request for inspection or audit.