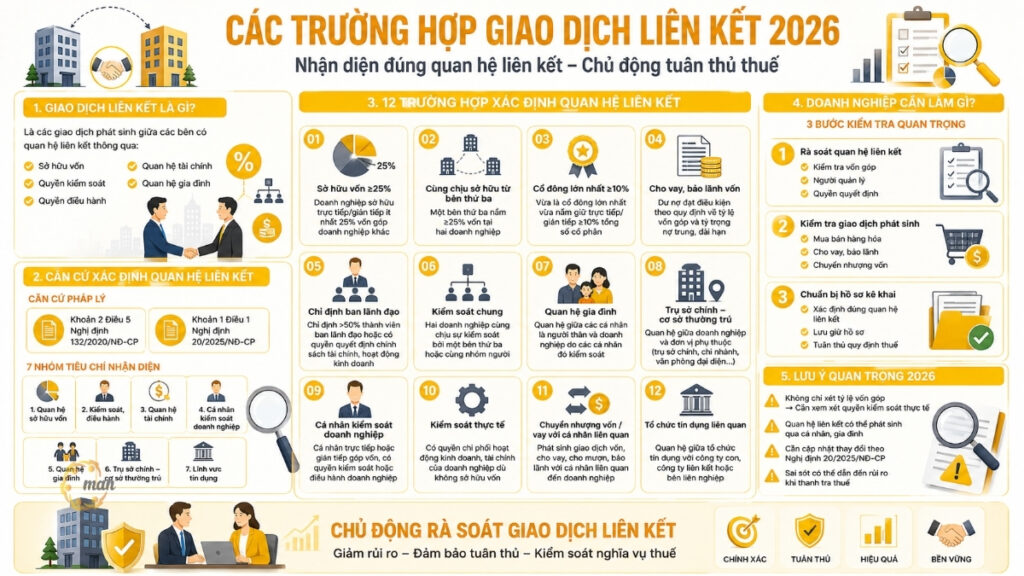

Interest expense for businesses affiliate transactions become one of the key factors that directly affect the tax obligations and compliance risks of enterprises. According to Decree 132/2020/ND-CP Regulations on interest expenses for enterprises with related transactions are as follows:

- The loan amount is at least 25% of equity and this loan accounts for more than 50% of the total value of medium and long-term debts.

- Compare the loan amount with the owner's equity at the time of the loan to determine whether the loan represents 25% or more of the owner's equity.

- Medium and long-term debt is debt with a payment term of 12 months or more or exceeding a business production cycle, including long-term loans, determined at the time of preparing the financial statements (FS).

- If the total loan from multiple parties reaches over 25% of equity but each individual party does not reach this level, it is not considered an affiliated transaction.

Therefore, accurately determining interest expenses for businesses with related-party transactions not only helps optimize tax obligations but also ensures transparency and compliance with international standards on anti-transfer pricing.

Regulations on interest expenses for enterprises with related transactions

During the operation process, businesses often need to borrow capital from banks or individuals to maintain production and business activities. However, not all loans are limited to financial aspects, but many cases are also directly related to regulations on interest costs for businesses with related transactions, requiring businesses to strictly comply with Decree 132/2020/ND-CP.

How to determine if a business has related-party transactions in the case of borrowing capital from a bank, and when is a loan considered a related-party transaction under the law?

Full information about affiliate relationships at: Identify the relationship

Regulations on interest expenses for enterprises with related transactions are specifically stipulated as follows.

For businesses borrowing from other businesses or credit institutions (banks)

To determine interest expenses for businesses with related transactions, it is necessary to base on specific legal criteria:

- According to regulations, during the fiscal year, if an enterprise borrows from a credit institution or another entity with a loan value of at least 25% of equity and at the same time this loan accounts for more than 50% of total medium and long-term debt, the enterprise is considered to have an affiliated transaction. Only when both conditions are satisfied, the loan is considered an affiliated transaction; if only one of the two conditions is satisfied, it is not considered an affiliated transaction.

- The comparison of the 25% equity ratio is made based on equity figures at the time of the loan. Meanwhile, medium and long-term debts are understood as those with a payment term of 12 months or more or exceeding a normal production - business cycle (including long-term loans), and are determined at the time of closing the accounting books when preparing financial statements.

- In addition, in case an enterprise borrows from many banks or many different organizations and the total loan value reaches 25% of equity, but each lender individually does not reach this level, it is not considered an affiliated transaction.

Example 1: Company A has equity of 15 billion VND and it has not changed during the year. On September 25, 2024, the company borrowed capital from bank M with the disbursed loan amount of 4 billion VND. On October 26, 2024, the company continued to borrow from bank Z with the loan amount of 4.5 billion VND. As of December 31, 2021, the company's total medium and long-term debts were 10 billion VND.

In this case, although the company's total loan is 8.5 billion, accounting for more than 25% of equity and over 50% of medium and long-term debt, but according to each bank, both banks do not qualify as loans over 25% of equity. Therefore, banks M and Z do not have any related transactions with company A.

In case of borrowing money from a business or bank on a per-loan basis and the total amount of loans is eligible, there is an associated transaction.

Example 2: Conditions as example 1, in this case the loan capital of bank M is 8.5 billion, accounting for more than 25% of equity and more than 50% of medium and long-term debts, then company A and bank M have related transactions.

Are there any cases where bank loans do not generate related transactions?

The answer is yes, but on condition that the loan must be a pure loan transaction, without any guarantee, co-ownership or control from the related party.

For example: Company C borrowed 8 billion from the Bank to serve its business activities. In this case, there is no relationship between Company C and the Bank regarding ownership, investment or guarantee.

Therefore, this loan does not generate related transactions, so there is no need to declare according to the provisions of Decree 132/2020/ND-CP.

Interest expense for businesses with personal loan related transactions

To better understand how to determine and handle interest expenses for businesses with related transactions, let's explore with MAN - Master Accountant Network the case of interest expenses for businesses with related transactions of personal loans, details as follows:

- In case an enterprise incurs a loan from an individual who operates or controls the enterprise (e.g., the director, owner or any individual) with a value equal to at least 10% of the owner's equity at the time of occurrence, this loan transaction is considered an affiliated transaction. In that case, the interest expense for the enterprise with the affiliated transaction will be subject to adjustment and control according to legal regulations. For example, if the director lends the enterprise an amount of money greater than 10% of the owner's equity, this loan transaction is automatically determined as an affiliated transaction.

For example: Company X has equity of 17 billion VND. During the year, due to lack of working capital, the company borrowed 2.5 billion VND from director T with an interest rate of 7%/year. Because this loan accounts for more than 10% of equity, it is determined to be an affiliated transaction.

- If during the year an enterprise borrows money from an individual executive with a value exceeding 10% of the owner's capital contribution, even if the loan is repaid by the end of the year, this transaction is still determined to be an affiliated transaction.

For example: Company X paid 2 billion to the director. However, in this case, director T and company X still had related party transactions.

- If a business borrows money without interest from the director (only borrows money) but the loan value reaches 10% of equity or more, it is still determined to be an affiliated transaction.

For example: The director approved the interest-free loan, but the loan transaction is also considered an affiliated transaction.

New regulations on interest expenses for affiliated enterprises when borrowing from banks

Decree 20/2025/ND-CP officially took effect from March 27, 2025, amending the regulations excluding banks from the scope of determining the occurrence of related-party transactions when borrowing from banks. So, what are the new regulations? And how will businesses benefit?

In fact, Decree 20/2025/ND-CP, if an enterprise is considered to have affiliated relationship with the lender if the following two conditions are simultaneously satisfied:

- Loan amount from at least 25% equity capital of borrowing enterprise.

- Loans over 50% total value of medium and long-term debts of borrowing enterprises.

Between the borrowing enterprise and the receiving enterprise belongs to one of the following relationships:

- One party directly or indirectly participates in the management, control, capital contribution and investment of the other party.

- Both parties are subject to the management, control, capital contribution and investment of a third party.

Therefore, if an enterprise borrows capital from a bank that is related to the control, capital contribution or management of the borrowing enterprise (or where both are under the control of another organization), the loan is still considered to have arisen as an affiliated transaction.

What is new in Decree 20/2025/ND-CP amending the interest expense for enterprises with related transactions?

Starting from March 27, 2025, Decree 20/2025/ND-CP officially takes effect and brings about an important change that decides that Banks will no longer be identified as affiliated parties when lending capital to businesses, as long as they meet certain conditions.

Specifically, the new provisions in Decree 20/2025/ND-CP still maintain the conditions on loan capital ratio as mentioned above. Important exceptions for credit institutions.

Accordingly, no matter how large a scale a business borrows from a bank, it will not be determined to have incurred related-party transactions when borrowing if:

- The bank does not participate in the management, control, capital contribution or investment in the borrowing enterprise.

- Borrowing enterprises and banks are not subject to the same management, control, capital contribution or investment by a third party.

Therefore, as long as there is no relationship in terms of control, management or ownership between the bank and the enterprise, the loan from the bank will no longer be considered an affiliated transaction, no matter how large the loan value is.

Conclude

Interest expense for businesses with related-party transactions is one of the core issues when managing taxes and complying with Decree 132/2020/ND-CP. Businesses need to clearly understand the ratio of loan capital and equity as well as the conditions for related-party transactions to avoid the risk of cost exclusion, collection or penalties. A transparent loan management system, along with complete related-party transaction records, not only ensures compliance but also contributes to optimizing costs and strengthening the business's reputation in the market.

If your business is having trouble determining interest expenses for businesses with related-party transactions, let MAN – Master Accountant Network Consulting and providing comprehensive solutions, helping you feel secure in sustainable development.

Contact information

- Address: 19A, Street 43, Tan Thuan Ward, Ho Chi Minh City.

- Mobile/ Zalo: +84 (0) 903 428 622 (Ms. Ngan)

- E-mail: nguyenthikimngan@man.net.vn

Editorial Board: MAN – Master Accountant Network