In the operations of affiliated enterprises, transactions arising between affiliated enterprises include:

- Purchase, sale, exchange, rent, lease, borrow, lend, transfer, assign goods, tangible and intangible assets; provide services;

- Borrowing, lending, financial services, financial guarantees and other financial instruments;

- Agreement to jointly use resources such as assets, capital, labor and share costs

Effectively managing transactions arising between affiliated businesses helps businesses optimize operations, comply with the law and minimize tax risks.

What are the transactions arising between affiliated enterprises?

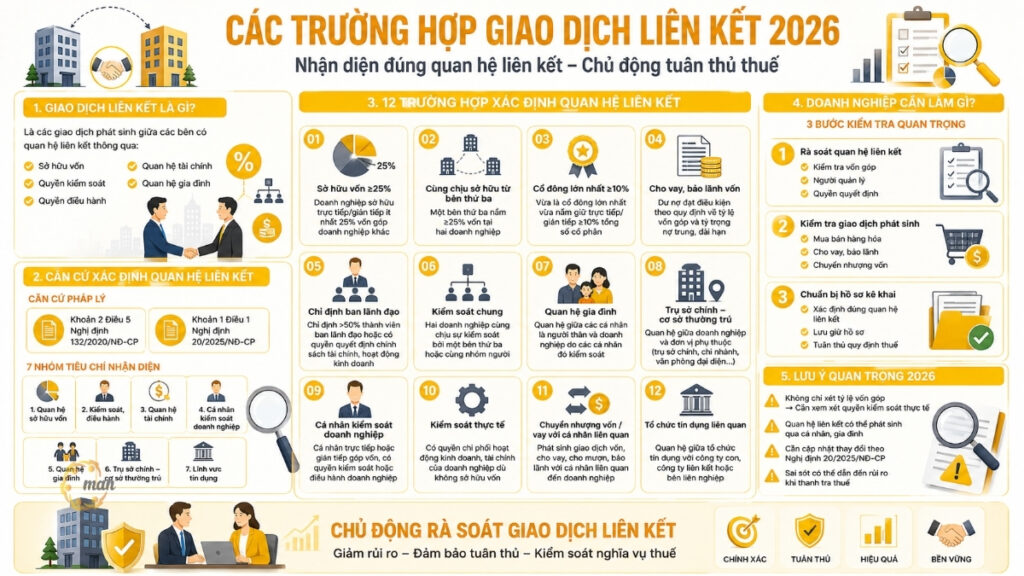

Transactions arising between affiliated enterprises are all activities of buying, selling, exchanging, leasing, borrowing, transferring or assigning goods, services, tangible and intangible assets between related companies. affiliated relationship regarding ownership, management or control. These transactions also include borrowing and lending, providing financial services, financial guarantees and other financial instruments, as well as agreements for the joint use of resources such as capital, assets, labor and cost sharing.

Identifying and effectively managing transactions arising between affiliated businesses is an important part of complying with legal regulations, especially Decree 132/2020/ND-CP on related party transaction management and tax risk prevention.

The importance of transactions arising between affiliated enterprises in risk management and tax compliance

In the process of managing transactions arising between affiliated enterprises, identifying, classifying and controlling transactions arising between affiliated enterprises is an important step. Specifically, as follows:

- Management affiliate transactions arising between affiliated enterprises is not only a legal obligation but also an important factor in risk management and tax compliance.

- Without proper control, transactions between associated businesses can create risks regarding valuation, cash flow and tax liability.

- Prepare complete records of transactions between affiliated enterprises, price them according to market principles and apply internal control measures.

- Help businesses comply with Decree 132/2020/ND-CP, reduce the risk of tax arrears, administrative penalties, ensure financial transparency, optimize business operations and build a solid foundation for sustainable development.

To clearly understand the responsibilities and obligations of enterprises, as well as apply effective management measures, it is necessary to first consider the legal basis regulating transactions arising between affiliated enterprises.

Legal basis related to transactions arising between affiliated enterprises

Under the current legal framework, transactions arising between affiliated enterprises are regulated in detail by Decree 132/2020/ND-CP and related guiding documents. These regulations clearly define the threshold and types of related transactions that must be reported, including transactions of purchase, sale, exchange, lending, provision of services, transfer of assets or agreements on shared use of resources between related parties.

Therefore, it is the responsibility of enterprises to prepare complete, accurate and timely records of related-party transactions, ensuring that information on prices, transaction conditions and related-party relationships are recorded transparently. Strict compliance with the requirements on records and reports not only helps enterprises meet their legal obligations, but also minimizes the risk of tax arrears, administrative fines and enhances financial transparency. At the same time, strictly managing transactions arising between related-party enterprises also helps enterprises optimize business operations and manage risks effectively.

Types of transactions arising between affiliated enterprises

In business practice, transactions between affiliated enterprises are often diverse and complex, requiring strict management to ensure compliance with the law and minimize tax risks. Some typical types of transactions include:

- Transfer of goods and services between affiliated companies: These are the most common transactions, directly affecting the revenue, costs and profits of each party.

For example: A manufacturing corporation has subsidiary A selling raw materials to subsidiary B at a market price of VND 10 billion in 2024. Accurate recording and filing ensures these transactions are transparent and avoids tax disputes.

- Borrowing – lending, guaranteeing, internal credit granting: These internal financial transactions help businesses optimize cash flow but at the same time create risks if not priced and managed according to market principles.

For example: The parent company provided a loan of VND5 billion to the subsidiary with an interest rate equivalent to the market interest rate; complete documents help prove legality and reduce the risk of tax arrears.

- Profit sharing, administrative and shared expenses: These transactions include the allocation of common expenses, administrative expenses or profit sharing among affiliated companies.

For example: The management cost of VND 2 billion is allocated to subsidiaries based on revenue ratio, ensuring accurate reflection of costs and reasonable profits according to regulations.

Identifying, classifying and documenting in detail transactions arising between affiliated enterprises not only helps enterprises comply with Decree 132/2020/ND-CP, but also enhances financial transparency, minimizes tax risks and creates a solid foundation for internal governance and sustainable development.

Risks related to transactions arising between affiliated enterprises

In corporate governance, transactions between affiliated businesses always pose many risks if not strictly controlled. In particular:

- Tax risks: If transactions between affiliated enterprises are not priced according to market principles or are not fully documented according to Decree 132/2020/ND-CP, enterprises are at risk of being subject to tax collection and administrative fines by tax authorities. For example, transferring goods at a price lower than market price may result in collection of the difference between value added tax (VAT) and corporate income tax (CIT).

- Financial risks: Transactions between affiliated businesses that are not transparent can affect the cash flow and liquidity of the business. For example, loans or internal guarantees that are not carefully managed can cause cash flow bottlenecks, reduce liquidity and affect business operations.

- Legal risks and weak internal controls: Lack of adequate control, monitoring and documentation of related-party transactions can lead to legal disputes, violations of internal governance regulations and impact on corporate reputation.

Thoroughly identifying and managing these risks in transactions arising between affiliated enterprises helps enterprises comply with the law, optimize cash flow, improve financial transparency and strengthen the foundation of sustainable risk management.

Control and manage transactions arising between affiliated enterprises

Effectively managing transactions between affiliated businesses requires businesses to establish a strict, transparent and fully compliant internal control system. The main steps include:

- Establish standardized internal control procedures: Every business needs to develop clear policies and procedures to identify, approve, and track all related transactions. This process helps ensure that all transactions are fully recorded, transparent, and traceable when needed.

- Valuation of transactions at market prices: To avoid tax risks and disputes, all related party transactions must be valued at market prices. Accurate valuation helps to reflect the true value of the transaction while ensuring compliance with Decree 132/2020/ND-CP.

- Transfer pricing documentation (Master file, Local file, CbCR): A detailed record of transactions, valuation bases, related party relationships and transaction conditions. This record serves not only for compliance purposes but also as a basis for internal audit and tax authority assessment.

- Regular monitoring and internal audit: Enterprises need to periodically check related transactions, compare with records and reports, detect errors or potential risks early. The internal audit process helps increase transparency, minimize tax risks and improve corporate governance efficiency.

The synchronous application of these steps helps businesses not only fully comply with legal regulations, but also optimize risk management, enhance transparency and ensure that all transactions arising between affiliated businesses are managed effectively and safely.

Conclude

Effectively managing transactions between affiliated enterprises not only helps enterprises strictly comply with Decree 132/2020/ND-CP, but also enhances financial transparency, minimizes tax risks and optimizes internal governance. Complete documentation, market valuation and regular monitoring are key to ensuring that all internal transactions are transparent, reasonable and safe.

To deploy an effective affiliate transaction management system, optimize legal compliance and minimize risks, businesses can contact MAN – Master Accountant Network for comprehensive advice and support, from documentation to transaction control and monitoring.

Contact information

- Address: 19A, Street 43, Tan Thuan Ward, Ho Chi Minh City.

- Mobile/ Zalo: +84 (0) 903 428 622 (Ms. Ngan)

- E-mail: nguyenthikimngan@man.net.vn

Editorial Board: MAN – Master Accountant Network