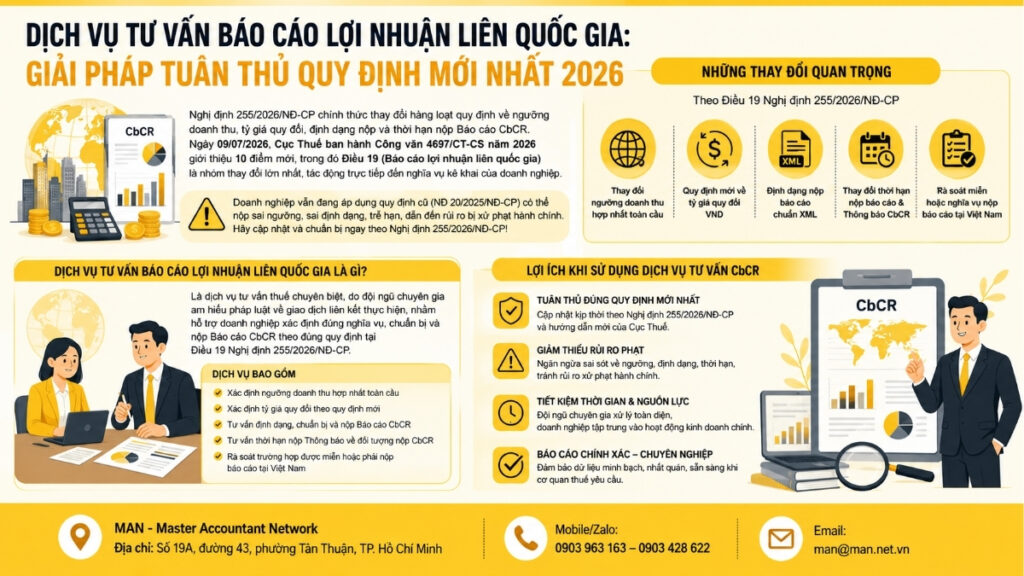

Pursuant to Clause 2, Article 5 Decree 132/2020/ND-CP, if an enterprise falls into one of the following cases, it is considered to have an affiliated relationship in an affiliated transaction. The table below will summarize in detail the criteria for forming an affiliated relationship.

Board: Summary of criteria for determining linkage relationships

| Numerical order | Affiliated Parties |

| 1 | 01 enterprise directly or indirectly holds at least 25% of the capital contribution of the owner of the other enterprise. |

| 2 | Both enterprises have at least 25% of owner's equity held directly or indirectly by third parties. |

| 3 | 01 enterprise is the largest shareholder in terms of owner's equity and directly or indirectly holds at least 10% of the total shares of the other enterprise. |

| 4 | 01 enterprise guarantees or lends capital to another enterprise in any form (including loans from third parties guaranteed by the financial resources of the associated party and financial transactions of similar nature) with the condition that the loan amount is at least equal to 25% of contributed capital over 50% of the total value of medium and long-term debts of the borrowing enterprise. Medium term: Over 01 year – 05 years. Long term: Over 05 years |

| 5 | One enterprise appoints a member of the executive board or controlling authority of another enterprise, provided that the number of members appointed by the first enterprise accounts for more than 50% of the total number of members of the executive board or controlling authority of the second enterprise; or a member appointed by the first enterprise has the right to decide on the financial policies or business operations of the second enterprise. |

| 6 | 02 enterprises have more than 50% members of the board of directors or have 01 member of the board of directors with the right to decide on financial policies or business operations appointed by a third party. |

| 7 | 02 Enterprises are operated or controlled in terms of personnel, finance and business activities by individuals in one of the following relationships: husband and wife; biological parents, adoptive parents, step-parents, step-mothers, parents-in-law; biological children, adopted children, step-children of the wife or husband, daughter-in-law, son-in-law; full siblings, half-siblings, half-siblings; brother-in-law, brother-in-law, sister-in-law of the same parents or half-siblings, paternal grandparents, maternal grandparents; paternal grandchildren, maternal grandchildren; paternal aunts, paternal uncles, paternal uncles, paternal uncles and paternal nieces and nephews. |

| 8 | 02 business establishments have a head office and permanent establishment relationship or are both permanent establishments of foreign organizations or individuals. |

| 9 | One or more enterprises are controlled by one individual through the capital contribution of this individual to that enterprise, or directly participating in the operation of the enterprise. |

| 10 | Other cases in which the enterprise is subject to the management, control and decision-making in practice regarding the production and business activities of the other enterprise. |

| 11 | The enterprise has transactions of transferring or receiving the transfer of at least 251 TP3T of capital contributions of the enterprise's owner during the tax period; borrowing or lending at least 101 TP3T of capital contributions of the owner at the time of the transaction during the tax period with the individual operating or controlling the enterprise, or with an individual in one of the related relationships as prescribed in point "7" of this clause. |

The above criteria show that the affiliated relationship does not only arise from the capital contribution ratio but also appears through many other factors such as management, operation, borrowing - lending (medium and long term) or business dependence. Enterprises need to regularly review according to these criteria to promptly identify, declare and prepare affiliated transaction records in accordance with regulations, thereby limiting tax risks and improving transparency in governance.

What is the affiliated relationship under Decree 132/2020/ND-CP?

Affiliate relationships play a fundamental role in helping businesses comply with tax laws, especially in the management aspect. affiliate transactions and transfer pricing prevention. In practice, the number of transactions between companies in the same group or with partners with ownership and control relationships is increasing, making the identification of related relationships urgent.

The important point is that determining an affiliated relationship does not stop at the capital contribution ratio, but also requires a comprehensive assessment of the governing factors such as financial guarantees, management rights, loan contracts or the right to decide on business policies. For example, if enterprise A only holds 25% of capital in enterprise B but has the right to appoint the CFO and approve large contracts, then according to tax law, this is still considered an affiliated relationship.

Correctly identifying an affiliated relationship requires clearly defined legal criteria and relevant records, documents, and contracts as a basis. These criteria are specifically stipulated in Decree 132/2020/ND-CP and reflect many different aspects: from capital ownership ratio, management rights, loan-borrowing relationships to dependence in business operations. Understanding and correctly applying the criteria for identifying affiliated relationships will help businesses make transactions transparent, minimize tax risks, and enhance governance reputation.

11 practical cases illustrating the relationship based on Decree 132/2020/ND-CP

Understanding the criteria is fundamental, but to better visualize how to apply them in business life, MAN – Master Accountant Network Let's take a look at some practical examples of common affiliated relationships. These illustrations will help businesses identify them more easily and clearly, avoiding confusion in the process of declaring and complying with tax laws.

Case 1: An enterprise directly or indirectly owns more than 25% of capital contributions of another enterprise.

Based on case 1 quote:

“01 enterprise directly or indirectly holds at least 25% of the capital contribution of the owner of the other enterprise”

ABC Vietnam Company operates in the field of electronic components manufacturing, with a charter capital of 100 billion VND. In which, XYZ Japan Company directly contributes 30 billion VND, equivalent to 30% of charter capital.

According to the provisions of Decree 132/2020/ND-CP, because company XYZ holds more than 25% of capital contribution in company ABC. Therefore, the two parties are determined to have an affiliated relationship. This means that all transactions arising between company ABC and company XYZ (for example: purchasing raw materials, paying technology copyright fees) must be declared as affiliated transactions and have a price determination dossier prepared according to regulations.

Case 2: Two enterprises have a common third-party owner holding 25% or more of contributed capital (directly or indirectly)

Based on case 2 quotes:

“Both enterprises have at least 25% of owner's equity held directly or indirectly by third parties.”

Company A and Company B both have the same owner, Group X. Of which, Group X holds 40% of capital contribution in Company A and at the same time Group X also holds 35% of capital contribution in Company B.

Although Company A and Company B do not directly contribute capital to each other, both have more than 25% of contributed capital held by the same owner (Group X). According to Decree 132/2020/ND-CP, this is determined to be an affiliated relationship through a third party.

Therefore, Company A and Company B are required to declare related-party transactions if they purchase, sell, borrow capital or provide services to each other, because this relationship satisfies the criteria of "being under the control of the same owner".

Case 3: The largest shareholder holds at least 10% of direct or indirect shares of another enterprise.

Based on case 3 quotes:

“01 enterprise is the largest shareholder in terms of owner's equity and directly or indirectly holds at least 10% of the total shares of the other enterprise.”

Company A contributed capital to Joint Stock Commercial Company B and became the largest shareholder, directly holding 17% of total voting shares. Although the ownership ratio has not reached 25% as some other criteria, according to the provisions of Decree 132/2020/ND-CP, the fact that an enterprise holds 10% or more shares is enough to determine that there is an affiliated relationship.

As the largest shareholder, Company A has the ability to control a significant part of the business activities of Joint Stock Commercial Company B, especially in financial decisions and development orientation. Therefore, all transactions arising between Company A and Joint Stock Commercial Company B (such as internal loans, service provision, asset transfer) are considered related party transactions, and need to be declared and recorded to determine the price according to the law.

Case 4: Enterprises guarantee or lend ≥25% of contributed capital and over 50% of medium/long-term debt.

Based on case 4 quotes:

“01 enterprise guarantees or lends capital to another enterprise in any form (including loans from third parties guaranteed by the financial resources of the associated party and financial transactions of similar nature) with the condition that the loan amount is at least equal to 25% of contributed capital over 50% of the total value of medium and long-term debts of the borrowing enterprise.”

Company M (parent company) directly lends Company N (subsidiary) VND 120 billion with a term of 4 years (medium term). Company N has equity of VND 400 billion, total medium and long-term debt of VND 200 billion (including VND 120 billion borrowed from Company M and VND 80 billion borrowed from a third party).

The VND 120 billion loan from company M accounts for 301.3 billion of company N's capital contribution. At the same time, this VND 120 billion loan accounts for 601.3 billion of company N's total medium and long-term debt.

From there, Company M and Company N are determined to have an affiliated relationship, because the loan satisfies both conditions.

Case 5: An enterprise has an affiliated relationship if it appoints more than 50% leaders or a designated leader decides on the financial or operational policies of another enterprise.

Based on case 5 quotes:

“One enterprise appoints a member of the executive board or controlling authority of another enterprise, provided that the number of members appointed by the first enterprise accounts for more than 50% of the total number of members of the executive board or controlling authority of the second enterprise; or a member appointed by the first enterprise has the right to decide on the financial policies or business operations of the second enterprise.”

Company X invested and invested in joint stock company Y, holding 40% of contributed capital. Currently, joint stock company Y has 5 members in the Board of Directors. Because it holds a high proportion of contributed capital, company X has the right to appoint 3 members out of the total 5 members of the Board of Directors of company Y. One of the members appointed by company X concurrently holds the position of Chairman of the Board of Directors and CEO, with the right to decide all business activities of company Y.

Company X and company Y have an affiliated relationship.

Case 6: Two businesses jointly control the board of directors or have a third-party appointed leader with the power to make financial or business decisions.

Based on case 6 cited:

“02 enterprises have more than 50% members of the board of directors or have 01 member of the board of directors with the right to decide on financial policies or business operations appointed by a third party.”

Company X and Company Y are two independent legal entities, each with 5 members in the Board of Directors. However, both companies have 3 out of 5 members directly appointed by Group Z (a third party), accounting for 60% of seats in the management apparatus. In particular, a member appointed by Group Z at Company X also holds the position of Chairman of the Board of Directors at Company Y, with full authority to decide on financial policies and business orientation. In this case, although X and Y do not cross-own capital, because they both have more than 50% members of the Board of Directors appointed by a third party and have at least one person holding the right to decide on policies at both companies, according to Decree 132/2020/ND-CP, Company X and Company Y are determined to have an affiliated relationship.

Case 7: Two businesses have an affiliated relationship when their operations, finances or business activities are influenced by individuals with direct family or close relatives.

Based on case 7 cited:

“02 enterprises are operated or controlled in terms of personnel, finance and business activities by individuals in one of the following relationships: husband and wife; biological parents, adoptive parents, step-parents, step-mothers, parents-in-law; biological children, adopted children, step-children of the wife or husband, daughter-in-law, son-in-law; full siblings, half-siblings, half-siblings; brother-in-law, brother-in-law, sister-in-law of the same parents or half-siblings, paternal grandparents, maternal grandparents; paternal grandchildren, maternal grandchildren; paternal aunts, paternal uncles, paternal uncles, paternal uncles and paternal nieces and nephews.”

Company X (pharmaceutical manufacturing) and Company Y (pharmaceutical distribution). The General Director of Company X is Mr. Nguyen Van A, while the Financial Director of Company Y is Ms. Nguyen Thi B. Mr. A and Ms. B are siblings. Although the two companies do not contribute capital or own shares to each other, because both businesses are operated and financially controlled by individuals with direct blood relations, tax law still determines this to be an affiliated relationship. This case shows that identification is not only based on capital contributions, but also needs to consider human factors and family relationships in corporate governance.

Case 8: 02 business establishments have a head office and permanent establishment relationship or are both permanent establishments of foreign organizations or individuals.

Case 8: 02 business establishments have a head office and permanent establishment relationship or are both permanent establishments of foreign organizations or individuals.

Group X is headquartered in Singapore and has established two permanent establishments in Vietnam, including a Representative Office in Hanoi and a Branch in Ho Chi Minh City. During the course of operation, these units may have many internal transactions such as allocating office expenses, sharing personnel, or transferring service contracts from the headquarters. According to the provisions of Decree 132/2020/ND-CP, the relationship between the headquarters and permanent establishments, as well as between two permanent establishments, are all determined to be affiliated relationships and must be fully declared and documented for affiliated transactions.

Case 9: The enterprise is controlled by the same individual through capital ownership or management rights

Based on case 9 cited:

“One or more enterprises are controlled by one individual through the capital contribution of this individual to that enterprise, or directly participating in the operation of the enterprise.”

Mr. Nguyen Van A is currently contributing capital and directly participating in management at many enterprises. Specifically, he owns 40% of charter capital and holds the position of Chairman of the Board of Directors at Company X, and holds 35% of charter capital and is the CEO at Company Y. With the capital contribution ratio both exceeding the threshold of 25% and the right to directly decide on business activities at both companies, Company X and Company Y are determined to have an affiliated relationship according to the law, because they are both under the control of a single individual.

Case 10: Enterprises are under the right to manage and control the production and business activities of other enterprises.

Based on case 10 quotes:

“Other cases in which the enterprise is subject to the management, control and decision-making in practice regarding the production and business activities of the other enterprise.”

Company X only owns 20% of capital in Company Y, lower than the prescribed threshold of 25%. However, the CEO and Chief Accountant of Company Y are both appointed by Company X, and all large contracts for purchasing raw materials as well as production plans must be approved by Company X. This shows that, although not holding a controlling capital ratio, Company X still controls the actual production and business activities of Company Y, and the two parties are still considered to have an affiliated relationship according to tax regulations.

Case 11: An affiliated relationship arises when an enterprise transfers from 25% capital contributions or borrows - lends from 10% capital contributions to individuals who operate, control or are associated according to regulations.

Based on case 11 cited:

“The enterprise has transactions of transferring or receiving the transfer of at least 251 TP3T of capital contributions of the enterprise owner during the tax period; borrowing or lending at least 101 TP3T of capital contributions of the owner at the time of the transaction during the tax period with the individual operating or controlling the enterprise, or with the individual in one of the related relationships as prescribed in point “7” of this clause.”

In the tax year 2025, Company X with a charter capital of VND 200 billion had two important transactions. First, a member of the Board of Directors transferred 30% of Company X's capital contribution to Company Y. Because this ratio exceeded the threshold of 25% of capital contribution, the transaction was considered the basis for forming an affiliated relationship according to regulations. Second, Company X borrowed VND 25 billion from its General Director to supplement working capital. This loan accounted for 12.5% of equity, higher than the 10% level prescribed by law, and the lender was an individual directly managing the enterprise. Thus, both transactions caused Company X and related parties to be identified as having an affiliated relationship, which means that the enterprise must declare and prepare a dossier of affiliated transactions according to Decree 132/2020/ND-CP.

Conclude

From the above analysis and examples, it can be seen that correctly identifying related relationships is not only a requirement to comply with tax laws but also an important tool for businesses to proactively manage risks, make transactions transparent and enhance their reputation with management agencies. In the context of increasingly strict regulations, businesses need to build a periodic review process and prepare related-party transaction documents professionally. If you want comprehensive support in identifying, declaring and preparing documents according to Decree 132/2020/ND-CP, please contact Ms. Ngan for advice on the most suitable and optimal solution for your business.

Contact information MAN – Master Accountant Network

- Address: 19A, Street 43, Binh Thuan Ward, District 7, Ho Chi Minh City.

- Mobile/ Zalo: +84 (0) 903 428 622 (Ms. Ngan)

- E-mail: nguyenthikimngan@man.net.vn

Editorial Board: MAN – Master Accountant Network