Giao dịch liên kết không chỉ là một thủ tục pháp lý, mà còn là cơ chế quan trọng giúp doanh nghiệp tuân thủ quy định về kê khai, xác định giá khi phát sinh quan hệ với bên liên quan. Đặc biệt, những doanh nghiệp có công ty mẹ, công ty con hoặc các đơn vị có quan hệ sở hữu, kiểm soát lẫn nhau cần nắm chắc quy định để tránh rủi ro pháp lý và nguy cơ bị xử phạt thuế.

If your business is having internal transactions but is not sure whether they are subject to declaration or not, then it is necessary to understand the concept, conditions for determining affiliated relationships and the obligation to declare according to the law. Decree 132/2020/ND-CP là điều không thể bỏ qua. Đồng thời, việc tham khảo dịch vụ lập hồ sơ giao dịch liên kết sẽ giúp doanh nghiệp đảm bảo tuân thủ pháp luật, tiết kiệm thời gian và giảm thiểu rủi ro.

In the context of integration and globalization, more and more Vietnamese enterprises are participating in multinational supply chains, leading to the need to allocate profits and costs among related parties. To effectively manage this activity, Vietnamese law has built a strict system of regulations that all enterprises must proactively comply with.

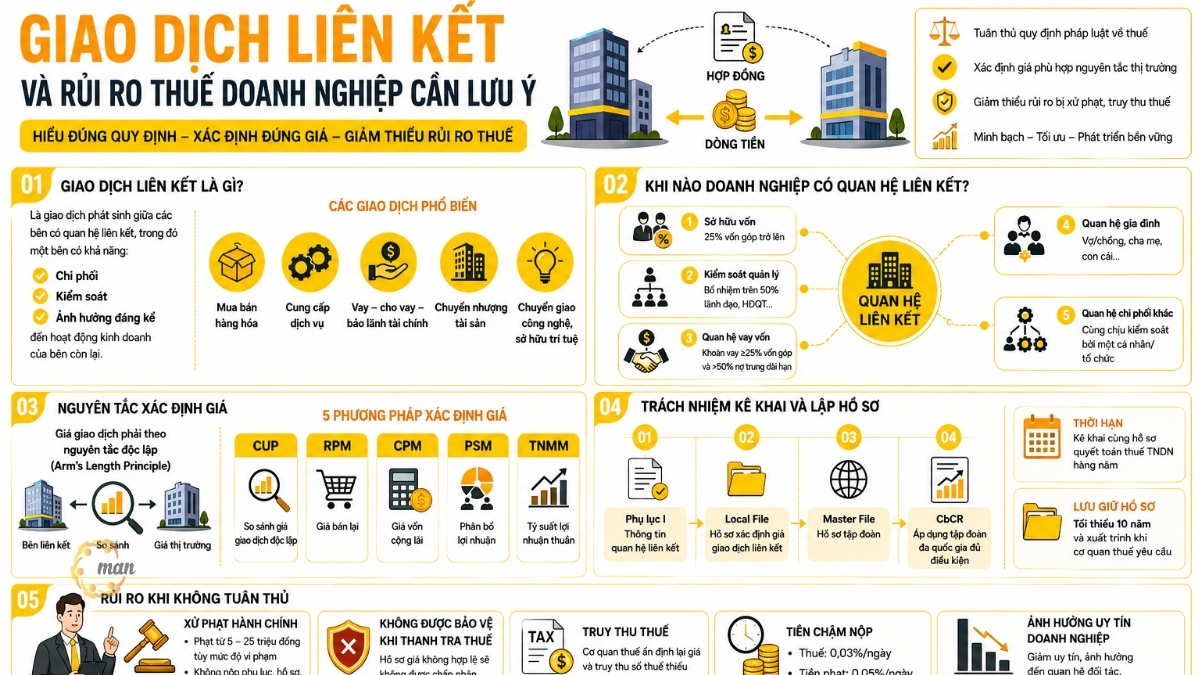

What is affiliate trading?

Theo Nghị định 132/2020/NĐ-CP của Chính phủ về quản lý thuế, giao dịch liên kết (tiếng Anh còn được gọi là Transfer Pricing) là những giao dịch phát sinh trong quá trình sản xuất, kinh doanh giữa các bên có quan hệ liên kết. Quan hệ liên kết ở đây là mối quan hệ mà một bên có khả năng chi phối, kiểm soát hoặc ảnh hưởng đáng kể đến điều kiện, chính sách hoặc kết quả kinh doanh của bên còn lại.

Các hoạt động giữa các bên có quan hệ liên kết có thể bao gồm:

- Buying and selling goods, providing and using services.

- Borrowing, lending, financial guarantee activities.

- Purchase or transfer of fixed assets.

- Transfer of intellectual property and technology.

- Allocation of costs or profits among related parties.

Affiliated transactions typically have the following characteristics:

- Không phải là giao dịch thường xuyên giữa các bên không có quan hệ liên kết trên thị trường;

- Có thể ảnh hưởng đến giá thành, doanh thu, lợi nhuận và thuế của các bên tham gia;

- Có thể được sử dụng để chuyển lợi nhuận từ một bên sang một bên khác để giảm thuế hoặc tối ưu hóa thuế.

Khi nào doanh nghiệp được xác định có quan hệ liên kết?

Căn cứ khoản 2 Điều 5 Nghị định 132/2020.NĐ-CP (được sửa đổi, bổ sung bởi khoản 1 Điều 1 Nghị định 20/2025/NĐ-CP), các trường hợp được hình thành mối quan hệ liên kết năm 2026 bao gồm:

- Một doanh nghiệp nắm giữ trực tiếp hoặc gián tiếp ít nhất 25% vốn góp của chủ sở hữu của doanh nghiệp kia.

- Cả hai doanh nghiệp đều có ít nhất 25% vốn góp của chủ sở hữu do một bên thứ ba nắm giữ trực tiếp hoặc gián tiếp.

- Một doanh nghiệp là cổ đông lớn nhất về vốn góp của chủ sở hữu và nắm giữ trực tiếp hoặc gián tiếp ít nhất 10% tổng số cổ phần của doanh nghiệp kia.

- Một doanh nghiệp bảo lãnh hoặc cho một doanh nghiệp khác vay vốn dưới bất kỳ hình thức nào (bao gồm cả các khoản vay từ bên thứ ba được đảm bảo từ nguồn tài chính của bên liên kết và các giao dịch tài chính có bản chất tương tự) với điều kiện tổng dư nợ các khoản vốn vay của doanh nghiệp đi vay với doanh nghiệp cho vay hoặc bảo lãnh ít nhất bằng 25% vốn góp của chủ sở hữu của doanh nghiệp đi vay và chiếm trên 50% tổng dư nợ tất cả các khoản nợ trung và dài hạn của doanh nghiệp đi vay.

- Một doanh nghiệp chỉ định thành viên ban lãnh đạo điều hành hoặc nắm quyền kiểm soát của một doanh nghiệp khác với điều kiện số lượng các thành viên được doanh nghiệp thứ nhất chỉ định chiếm trên 50% tổng số thành viên ban lãnh đạo điều hành hoặc nắm quyền kiểm soát của doanh nghiệp thứ hai; hoặc một thành viên được doanh nghiệp thứ nhất chỉ định có quyền quyết định các chính sách tài chính hoặc hoạt động kinh doanh của doanh nghiệp thứ hai.

- Hai doanh nghiệp cùng có trên 50% thành viên ban lãnh đạo hoặc cùng có một thành viên ban lãnh đạo có quyền quyết định các chính sách tài chính hoặc hoạt động kinh doanh được chỉ định bởi một bên thứ ba.

- Hai doanh nghiệp được điều hành hoặc chịu sự kiểm soát về nhân sự, tài chính và hoạt động kinh doanh bởi các cá nhân thuộc một trong các mối quan hệ gia đình (như vợ, chồng, cha mẹ ruột, cha me nuôi,…)

- Hai cơ sở kinh doanh có mối quan hệ trụ sở chính và cơ sở thường trú hoặc cùng là cơ sở thường trú của tổ chức, cá nhân nước ngoài.

- Các doanh nghiệp chịu sự kiểm soát của một cá nhân thông qua vốn góp của cá nhân này vào doanh nghiệp đó hoặc trực tiếp tham gia điều hành doanh nghiệp.

- Các trường hợp khác trong đó doanh nghiệp (bao gồm cả chi nhánh hạch toán độc lập thực hiện kê khai, nộp thuế thu nhập doanh nghiệp) chịu sự điều hành, kiểm soát, quyết định trên thực tế đối với hoạt động sản xuất kinh doanh của doanh nghiệp kia.

- Doanh nghiệp có phát sinh các giao dịch nhượng, nhận chuyển nhượng vốn góp ít nhất 25% vốn góp của chủ sở hữu của doanh nghiệp trong kỳ tính thuế; vay, cho vay ít nhất 10% vốn góp của chủ sở hữu tại thời điểm phát sinh giao dịch trong kỳ tính thuế với cá nhân điều hành, kiểm soát doanh nghiệp hoặc với cá nhân thuộc trong một các mối quan hệ gia đình như đã nêu trên.

- Tổ chức tín dụng với Công ty con hoặc với Công ty kiểm soát hoặc với Công ty liên kết của tổ chức tín dụng theo quy định tại Luật Các tổ chức tín dụng và các văn bản sửa đổi, bổ sung hoặc thay thế (nếu có).

Việc xác định đúng quan hệ liên kết chỉ là bước khởi đầu. Sau khi đã nhận diện mối quan hệ liên kết, doanh nghiệp bắt buộc phải thực hiện nghĩa vụ kê khai theo quy định pháp luật. Đây là yêu cầu quan trọng nhằm đảm bảo tính minh bạch trong quản lý thuế.

Nguyên tắc xác định giá trong các giao dịch giữa các bên liên quan

Khi phát sinh các giao dịch với bên liên quan, doanh nghiệp phải đảm bảo mức giá được xác định phù hợp với nguyên tắc độc lập và điều kiện thị trường. Hiểu một cách đơn giản, đây là nguyên tắc đảm bảo rằng giá giao dịch giữa các bên liên quan phải được xác lập tương đương với mức giá mà các bên độc lập (không có quan hệ liên kết) thỏa thuận với nhau trong điều kiện giao dịch tương tự. Nguyên tắc này giúp loại bỏ tình trạng chuyển giá và phản ánh đúng bản chất kinh tế của giao dịch.

According to Decree 132/2020/ND-CP, below are the main methods for businesses to apply when determining market prices:

Comparable Uncontrolled Price (CUP) Method

Phương pháp này bằng cách so sánh trực tiếp giá của giao dịch giữa các bên liên kết với giá của giao dịch tương tự giữa các bên độc lập. Điều kiện so sánh cần tương đồng về hàng hóa, dịch vụ, thị trường, số lượng, điều kiện thanh toán, thời điểm giao dịch… Phương pháp này thường phù hợp với các sản phẩm có tính phổ biến, dễ xác định giá thị trường.

For example: Công ty A tại Việt Nam mua 10.000 sản phẩm linh kiện từ công ty mẹ ở nước ngoài với giá 100 USD/sản phẩm. Trong cùng thời điểm, công ty mẹ cũng bán cùng loại linh kiện cho một khách hàng độc lập khác với giá 80 USD/sản phẩm trong điều kiện tương tự. Cơ quan thuế có thể xem xét mức giá 80 USD là giá giao dịch độc lập để đánh giá liệu giá mua từ công ty mẹ có phù hợp hay không.

Resale Price Method (RPM)

Phương pháp này bắt đầu từ giá bán lại sản phẩm cho khách hàng độc lập, sau đó trừ đi biên lợi nhuận gộp hợp lý của nhà phân phối và các chi phí liên quan để xác định giá mua từ bên liên kết. Phù hợp với doanh nghiệp thương mại, phân phối chỉ thực hiện các hoạt động đơn giản như lưu kho, marketing cơ bản, bán hàng.

For example: Công ty B tại Việt Nam mua điện thoại từ công ty mẹ với giá chưa xác định. Sau đó công ty B bán lại cho khách hàng trong nước với giá 10 triệu đồng/chiếc. Một nhà phân phối độc lập trên thị trường thường hưởng biên lợi nhuận gộp khoảng 20%. Giá mua hợp lý từ công ty mẹ có thể được xác định:

Giá mua từ công ty mẹ = Giá bán lại – (20% x Giá bán lại) = 10 triệu – (20% x 10 triệu) = 8 triệu đồng |

Cost plus method (CPM)

Phương pháp này xác định giá giao dịch bằng cách lấy tổng chi phí sản xuất hoặc cung cấp dịch vụ cộng thêm một tỷ suất lợi nhuận phù hợp mà doanh nghiệp độc lập trong điều kiện tương tự có thể đạt được. Thường dùng cho doanh nghiệp sản xuất gia công, cung cấp dịch vụ kỹ thuật hoặc sản xuất theo đơn đặt hàng.

For example: Công ty C tại Việt Nam sản xuất linh kiện cho công ty mẹ ở nước ngoài. Chi phí sản xuất gồm nguyên vật liệu, nhân công, khấu hao… là 5 tỷ đồng. Qua dữ liệu so sánh, các doanh nghiệp sản xuất độc lập thường đạt lợi nhuận 10% trên chi phí. Giá bán hợp lý cho công ty mẹ được xác định:

Giá bán cho công ty mẹ = Chi phí sản xuất + (Chí phí sản xuất x Phần trăm lợi nhuận) = 5 tỷ + (5 tỷ x 10%) = 5.5 tỷ đồng |

Phương pháp phân bổ lợi nhuận (PSM)

Phương pháp này áp dụng khi các bên tham gia cùng tạo ra giá trị đáng kể và khó xác định giao dịch độc lập tương đương. Tổng lợi nhuận tạo ra từ giao dịch sẽ được phân chia dựa trên mức độ đóng góp thực tế của từng bên về chức năng, tài sản sử dụng và rủi ro chịu trách nhiệm.

For example: Công ty X và công ty Y trong cùng tập đoàn cùng phát triển một sản phẩm công nghệ mới. Công ty X chịu trách nhiệm nghiên cứu, phát triển công nghệ; công ty Y phụ trách sản xuất và phân phối. Sau khi trừ chi phí, tổng lợi nhuận tạo ra là 100 tỷ đồng. Dựa trên mức đóng góp, công ty X được phân bổ 60% lợi nhuận (60 tỷ đồng), công ty Y nhận 40% (40 tỷ đồng).

Phương pháp tỷ suất lợi nhuận thuần (TNMM)

Phương pháp này so sánh mức lợi nhuận thuần mà một bên đạt được với mức lợi nhuận của các doanh nghiệp độc lập có chức năng tương tự. Đây là phương pháp được sử dụng phổ biến vì dễ tìm dữ liệu so sánh hơn so với phương pháp so sánh trực tiếp giá.

For example: Công ty D Việt Nam mua nguyên liệu từ công ty liên kết nước ngoài và sản xuất thành phẩm bán trong nước. Sau phân tích, các doanh nghiệp sản xuất độc lập tương tự có tỷ suất lợi nhuận thuần khoảng 5% doanh thu. Nếu công ty D chỉ đạt 1%, cơ quan thuế có thể xem xét điều chỉnh giá mua nguyên liệu hoặc các yếu tố liên quan để đưa lợi nhuận về mức phù hợp.

Doanh nghiệp cần lựa chọn phương pháp phù hợp nhất cho từng ngành nghề hoạt động. Đồng thời, doanh nghiệp phải lập hồ sơ, giải trình rõ cơ sở lựa chọn, cách áp dụng và nguồn dữ liệu tham chiếu, nhằm đảm bảo tính tin cậy khi cơ quan thuế kiểm tra.

Trách nhiệm kê khai và lập hồ sơ theo quy định

Theo quy định hiện hành, các đơn vị thuộc phạm vi điều chỉnh của quy định này phải thực hiện nghĩa vụ kê khai thông tin về quan hệ liên kết và các giao dịch phát sinh trong kỳ tính thuế. Nội dung kê khai được thể hiện tại Phụ lục I, II, III ban hành kèm Nghị định 132/2020/NĐ-CP, cụ thể:

Declaration of information on related relationships (Appendix I)

- Identify related parties based on criteria of capital, management, operations, human relations, family relations, etc.

- Statistics of all transactions occurring during the period with related parties.

See details: Phụ lục giao dịch liên kết.

Transfer pricing determination dossier

- Local file: Detailed analysis of operations, functions, risks, financial information of enterprises and related parties in Vietnam.

- Master file: General information of the entire corporation, organizational structure, transfer pricing policy, profit allocation.

- Country-by-Country Reporting (CbCR): Applicable to multinational corporations with global consolidated revenue of VND 18,000 billion or more.

Deadline for declaration and submission of documents

- Doanh nghiệp phải kê khai giao dịch liên kết cùng thời điểm nộp tờ khai quyết toán thuế thu nhập doanh nghiệp (TNDN) hàng năm.

- Hồ sơ xác định giá phải được lập, lưu giữ và xuất trình khi cơ quan thuế yêu cầu, với thời hạn tối thiểu 10 năm.

Hệ quả khi doanh nghiệp không tuân thủ

Administrative sanctions

Khi doanh nghiệp có quan hệ liên kết nhưng không kê khai, không lập hoặc không xuất trình Phụ lục và Hồ sơ xác định giá giao dịch liên kết theo Nghị định 132/2020/NĐ-CP, cơ quan thuế có quyền xử phạt vi phạm hành chính về thuế và ấn định số tiền thuế phải nộp (theo Luật Quản lý thuế và các nghị định hướng dẫn)

According to Decree 125/2020/ND-CP, những hành vi như không nộp phụ lục khi quyết toán thuế TNDN hoặc không nộp hồ sơ khai thuế có thể bị phạt tiền, cụ thể như sau:

“A fine of VND 5,000,000 to VND 8,000,000 shall be imposed for submitting tax declarations 31 to 60 days after the prescribed deadline.

A fine of from VND 8,000,000 to VND 15,000,000 shall be imposed for one of the following acts:

- Submitting tax declaration documents 61 to 90 days past the prescribed deadline;

- Submitting tax declaration documents 91 days or more after the prescribed deadline but no tax payable arises;

- Not submitting tax return but no tax payable;

- Failure to submit appendices as prescribed in tax management regulations for enterprises with related transactions attached to corporate income tax settlement dossiers.

A fine of VND 15,000,000 to VND 25,000,000 shall be imposed for the act of submitting a tax declaration more than 90 days after the deadline for submitting a tax declaration, with tax payable arising and the taxpayer having paid the full amount of tax and late payment to the state budget before the tax authority announces the decision to conduct a tax audit or inspection or before the tax authority makes a record of the act of late submission of a tax declaration.”

Risk of tax arrears

Pursuant to Clause 2, Article 59 of the Law on Tax Administration 2019, the rate of late tax payment and the time for calculating payment are as follows:

- The late payment fee is 0.03%/day calculated on the amount of late tax payment.

- The calculation period is calculated continuously from the day following the date of late payment as prescribed in Clause 1 of this Article to the day immediately preceding the date of tax debt.

Clause 1, Article 42 of Decree 125/2020/ND-CP stipulates the calculation of late payment fines as follows:

“Organizations and individuals who are late in paying administrative fines for tax and invoice violations will be charged a late payment fine of 0.05%/day calculated on the amount of late payment fine.

The number of days of late payment of fines includes holidays and days off according to regulations and is calculated from the day following the deadline for payment of fines to the day immediately preceding the day the organization or individual pays the fine to the state budget.”

Example: Coca-Cola VN bị cơ quan thuế yêu cầu phải nộp vào ngân sách hơn 821 tỉ đồng tiền truy thu thuế và phạt chậm nộp, nhiều chuyên gia cho rằng vẫn còn nhiều “ông lớn” FDI cần được đưa vào “tầm ngắm” thanh tra để chống chuyển giá, trốn thuế. Từ ví dụ thực tiễn cho thấy dù là doanh nghiệp lớn, nếu hồ sơ và cách xác định giá không thuyết phục, hậu quả về thuế và uy tín là rất nặng nề.

Source: Coca-Cola Vietnam's tax debt

Full compliance with legal regulations on related party transactions not only requires businesses to understand the legal framework, but also the ability to analyze, choose appropriate pricing methods and create transparent records. This is a complex process, requiring in-depth expertise in tax, accounting and practical experience in many industries. MAN – Master Accountant Network is confident to be a reliable companion in the field of related party transactions.

Summary table of contents on related party transactions according to Decree 132/2020/ND-CP

For easy reference, MAN – Master Accountant Network has systematized the core information about related party transactions in the following table.

| Topic | Main idea |

| Concept | Related party transactions are transactions arising between related parties, in which one party has the ability to dominate, control and significantly influence the other party. |

| Types of transactions | Buying and selling goods and services Borrow, lend, financial guarantee Buying, selling and transferring fixed assets Transfer of intellectual property and technology Cost and profit allocation |

| Characteristic | Not a regular market transaction Impact on cost, revenue, profit and tax Can be exploited for transfer pricing, tax reduction |

| In case of occurrence | Transactions within the same system (parent - child, branch) Transactions with a controlling or dominant party Transactions with relatives of the controlling party Transactions are controlled by one individual or organization. Deal with the designated party |

| Principles of price determination | Giá trong giao dịch liên kết phải theo nguyên tắc giá thị trường ( Arm’s Length) |

| Pricing method | Compare Independent Transaction Prices (CUP) Resale Price (RPM) Cost Plus Profit (CPM) Profit Distribution Metric (PSM) Self-trading price (TNMM) |

| Conditions for determining the relationship | Owned capital: 25% or more contributed capital Management and operation: Appointing more than 501 members of the Board of Directors, General Director... Loan or lending relationship of 25% or more contributed capital and greater than 50% medium and long-term debt Quan hệ nhân sự hoặc gia đình (cha mẹ, vợ chồng, con cái…) Intermediary/appointment relationship |

| Declaration obligation | Phụ luc I thông tin về các bên liên kết Local file Master file Cross-border profit reporting (CbCR, with a group of over 18,000 billion VND) |

| Term and retention | Kê khai cùng thời điểm nộp quyết toán thuế TNDN hàng năm (31/03) Keep records for at least 10 years |

| Risks of Non-Compliance | Bị xử phạt hành chính (5 – 25 triệu đồng tùy mức độ) Nguy cơ truy thu thuế và tính tiền chậm nộp (0.03%/ngày đối với thuế; 0.05%/ngày đối với phạt) và mất uy tín doanh nghiệp |

Qua bảng tổng hợp trên, có thể thấy giao dịch liên kết là một lĩnh vực phức tạp, đòi hỏi doanh nghiệp vừa nắm chắc quy định, vừa có chiến lược quản trị phù hợp. Đây cũng chính là lý do MAN – Master Accountant Network luôn đồng hành cùng doanh nghiệp để đảm bảo tuân thủ và tối ưu hiệu quả.

MAN – Master Accountant Network with over 30 years of experience in financial consulting and related transactions

With over 30 years of experience in the field of auditing and financial consulting, MAN – Master Accountant Network has become a trusted partner of thousands of small and medium enterprises and large corporations in Vietnam. The extensive experience not only helps MAN deeply understand the tax and accounting law system, but also understand the specifics of each industry. Thanks to that, all audit reports conducted by MAN – Master Accountant Network ensure accuracy, transparency and high legal value.

CPA, ACCA, Big4 background team

MAN – Master Accountant Network’s team of auditors includes CPAs, ACCAs and experts who have worked at Big4 companies. The combination of solid professional background and multi-industry practical experience provides customers with standardized, rigorous auditing processes that meet the strict requirements of both domestic and FDI enterprises.

VACPA member, complying with international standards

MAN – Master Accountant Network is a member of the Vietnam Association of Certified Public Accountants (VACPA) and complies with international accounting and auditing standards (VAS, ISA). This not only ensures the transparency of financial reports but also helps businesses feel confident when participating in international transactions, raising capital, or working with credit institutions.

Conclude

Transfer pricing is a complex financial legal issue, associated with many tax risks if businesses do not identify and declare correctly according to regulations. Understanding the conditions for determining and complying with the obligation to declare and prepare documents not only helps businesses avoid penalties, but also creates a transparent and sustainable management foundation in the long term. In the context of tax authorities increasingly tightening the management of transfer pricing activities, businesses need to proactively seek consulting solutions and support from reputable units to ensure compliance with the law and optimize resources.

Contact MAN – Master Accountant Network để được hỗ trợ và tư vấn miễn phí!

Contact information MAN – Master Accountant Network

- Address: Số 19A, Đường 43, Phường Tân Thuận, TP. Hồ Chí Minh

- Mobile/Zalo: 0903 963 163 – 0903 428 622

- E-mail: man@man.net.vn

- Google Business Profile: Xem Google Business Profile của MAN – Master Accountant Network

- LinkedIn Founder: Xem hồ sơ LinkedIn của chuyên gia Lê Hoàng Tuyên

Phụ trách sản xuất và kiểm duyệt nội dung chuyên môn bởi: Ông Lê Hoàng Tuyên – Sáng lập viên (Founder) & CEO MAN – Master Accountant Network. Ông là Kiểm toán viên CPA Việt Nam với hơn 30 năm kinh nghiệm sâu sắc trong lĩnh vực Kế toán, Kiểm toán, Thuế và Tư vấn Pháp lý doanh nghiệp.

Câu hỏi thường gặp về giao dịch liên kết

Có. Trường hợp doanh nghiệp Việt Nam giao dịch với công ty mẹ ở nước ngoài và đáp ứng điều kiện về quan hệ liên kết thì doanh nghiệp thuộc diện phải kê khai giao dịch liên kết và có thể phải lập hồ sơ xác định giá giao dịch liên kết. Hồ sơ cần thể hiện cơ sở xác định giá, phân tích chức năng, tài sản và rủi ro (FAR) và phương pháp xác định giá phù hợp.

Không phải mọi trường hợp đều bắt buộc lập đầy đủ hồ sơ. Doanh nghiệp có thể được miễn lập hồ sơ xác định giá giao dịch liên kết nếu đáp ứng các điều kiện miễn trừ theo quy định. Tuy nhiên, doanh nghiệp vẫn phải kê khai thông tin giao dịch liên kết theo quy định trong hồ sơ quyết toán thuế thu nhập doanh nghiệp.

Doanh nghiệp kê khai giao dịch liên kết cùng thời điểm nộp hồ sơ quyết toán thuế thu nhập doanh nghiệp hàng năm thường là 31/03. Thông tin giao dịch liên kết được kê khai trên các phụ lục liên quan ban hành kèm theo Nghị định 132/2020/NĐ-CP.

Theo Điểm g Khoản 2 Điều 5 Nghị định 132/2020/NĐ-CP quan hệ liên kết phát sinh khi hai doanh nghiệp cùng được điều hành hoặc chịu sự kiểm soát về nhân sự, tài chính và hoạt động kinh doanh bởi các cá nhân có quan hệ gia đình, trong đó có quan hệ vợ chồng. Điểm mấu chốt nằm ở chủ thể, quy định chỉ áp dụng cho mối quan hệ giữa hai doanh nghiệp. Trong khi đó, hộ kinh doanh không phải là doanh nghiệp theo pháp luật hiện hành. Vì vậy, trường hợp một bên là doanh nghiệp (do chồng làm chủ) và một bên là hộ kinh doanh (do vợ làm chủ) không thuộc các trường hợp được liệt kê là bên có quan hệ liên kết.Công ty có giao dịch với công ty mẹ ở nước ngoài có phải lập hồ sơ giao dịch liên kết không?

Phát sinh giao dịch liên kết có bắt buộc phải lập hồ sơ xác định giá không?

Thời hạn kê khai giao dịch liên kết là khi nào?

Giao dịch giữa chồng chủ doanh nghiệp và vợ chủ hộ kinh doanh có phát sinh giao dịch liên kết không?