Quy định về giao dịch liên kết đang là tâm điểm chú ý của cộng đồng doanh nghiệp khi cơ quan thuế ngày càng siết chặt kiểm soát hoạt động chuyển giá. Việc nắm vững và tuân thủ đúng quy định không chỉ giúp doanh nghiệp tránh rủi ro truy thu, xử phạt thuế, mà còn góp phần đảm bảo minh bạch tài chính, tuân thủ Decree 132/2020/ND-CP và chuẩn mực OECD. Bài viết dưới đây sẽ giúp doanh nghiệp hiểu rõ khung pháp lý, nghĩa vụ kê khai Phụ lục, Transfer pricing determination dossier, cùng những điểm quan trọng trong năm 2026 để doanh nghiệp chủ động phòng ngừa rủi ro và tối ưu nghĩa vụ thuế hợp pháp.

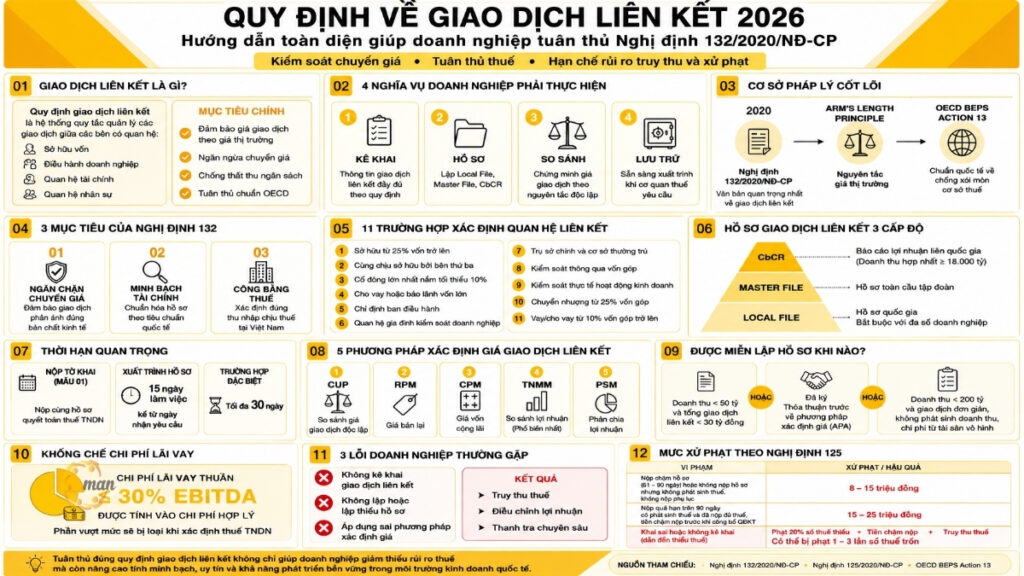

Quy định giao dịch liên kết là gì?

Quy định giao dịch liên kết là hệ thống các quy tắc pháp lý do Chính phủ và Bộ Tài chính ban hành, nhằm quản lý và kiểm soát các giao dịch giữa các bên có quan hệ liên kết tức là các doanh nghiệp có mối quan hệ sở hữu, điều hành hoặc phụ thuộc về tài chính, vốn, nhân sự.

Theo Nghị định 132/2020/NĐ-CP, các quy định này giúp đảm bảo giá giao dịch giữa các bên liên kết phản ánh đúng giá thị trường (nguyên tắc độc lập), ngăn chặn hành vi chuyển giá để trốn thuế hoặc giảm thu nhập chịu thuế tại Việt Nam.

Simply put, regulations on related party transactions are a legal framework that requires businesses with related party relationships to:

- Fully declare information on related transactions

- Prepare transfer pricing documents (Master file, Local file, CbCR)

- Comply with market price principles

Quy định giao dịch liên kết chính là công cụ giúp cơ quan thuế phát hiện, ngăn ngừa chuyển giá và giúp doanh nghiệp thực hiện đúng nghĩa vụ thuế, tránh rủi ro pháp lý trong bối cảnh hội nhập quốc tế.

Core legal basis for the regulation of related party transactions

Compliance with regulations on related party transactions in Vietnam is mainly regulated by the following legal documents:

Decree 132/2020/ND-CP regulating related-party transactions

Decree No. 132/2020/ND-CP of the Government, issued on November 5, 2020, is the most comprehensive and detailed legal document on tax management for enterprises with related-party transactions. This Decree replaces Decree 20/2017/ND-CP, overcomes limitations on controlling loan interest expenses and clarifies documents and methods for determining prices.

Việc hiểu rõ Nghị định 132 là yêu cầu bắt buộc để tuân thủ quy định về giao dịch liên kết hiện hành. Vì tính chất phức tạp của giao dịch và rủi ro truy thu ấn định thuế cao, cho nên nhiều doanh nghiệp đã lựa chọn tham khảo dịch vụ tư vấn giao dịch liên kết nhằm rà soát quan hệ liên kết, đánh giá rủi ro thuế và xây dựng phương án tuân thủ phù hợp với đặc thù hoạt động kinh doanh.

Principle of independent trading

This is the fundamental and essential principle governing all regulations on related-party transactions, built on international practice. The core content of this principle is expressed through the following points:

- Accordingly, the price of related-party transactions must be determined through analysis and comparison with equivalent independent transactions (transactions between unrelated parties).

- Decree 132 affirms: The value of an associated transaction is considered inconsistent with an independent transaction if it is established for the purpose of reducing the corporate income tax liability payable in Vietnam.

Objectives of Decree 132/2020/ND-CP regulating related-party transactions

Quy định giao dịch liên kết theo Nghị định 132/2020/NĐ-CP được xây dựng dựa trên Nguyên tắc giá thị trường (Arm’s Length Principle) và hướng dẫn BEPS Action 13 của OECD, với ba mục tiêu chính:

- Prevent transfer pricing: Ensure transactions between related parties are properly valued at market value, reflecting their true economic nature.

- Increase financial transparency: Require businesses to clearly declare and establish documents proving related-party transactions according to international standards.

- Ensuring fairness in tax obligations: Helping tax authorities correctly determine taxable income in Vietnam, avoiding budget losses.

According to the General Department of Taxation, since Decree 132 regulating related-party transactions was applied, many FDI enterprises have had to adjust and reduce unreasonable costs and supplement documents to determine related-party transaction prices.

Phạm vi áp dụng quy định về giao dịch liên kết

Trước khi áp dụng các quy định về giao dịch liên kết, doanh nghiệp phải xác định liệu mình có thuộc phạm vi của quan hệ liên kết hay không. Theo Khoản 2, Điều 5 Nghị định 132/2020/NĐ-CP, doanh nghiệp được xác định là có quan hệ liên kết khi thuộc 01 trong 11 trường hợp cụ thể dưới đây:

- An enterprise directly or indirectly holds at least 25% of equity capital of the other enterprise.

- Both businesses have at least 25% of equity held directly or indirectly by a third party.

- One enterprise is the largest shareholder in terms of equity and directly or indirectly holds at least 10% of the equity of the other enterprise.

- An enterprise guarantees or lends capital to another enterprise on the condition that the loan accounts for at least 25% of equity and accounts for more than 50% of total value of long-term debts.

- Một doanh nghiệp chỉ định thành viên Ban lãnh đạo điều hành hoặc nắm quyền kiểm soát với điều kiện số lượng thành viên được doanh nghiệp thứ nhất chỉ định chiếm trên 50% tổng số thành viên Ban lãnh đạo điều hành doanh nghiệp thứ hai. Hoặc thành viên được doanh nghiệp thứ nhất chỉ định có quyền quyết định các chính sách tài khóa và hoạt động kinh doanh.

- Hai doanh nghiệp được điều hành hoặc chịu sự kiểm soát về nhân sự, tài chính và hoạt động kinh doanh bởi các cá nhân thuộc một trong các mối quan hệ như vợ, chồng, cha, mẹ, con, anh, chị, em…

- The two businesses have a head office and permanent establishment relationship, or both are permanent establishments of a foreign organization or individual.

- Chịu sự kiểm soát của một cá nhân thông qua vốn góp hoặc trực tiếp tham gia điều hành

- Các trường hợp khác như doanh nghiệp chịu sự điều hành, kiểm soát, quyết định trên thực tế đối với hoạt động sản xuất kinh doanh của doanh nghiệp kia.

- Có phát sinh các giao dịch nhượng, nhận chuyển nhượng vốn góp ít nhất 25% vốn góp của chủ sở hữu của doanh nghiệp trong kỳ tính thuế.

- Vay, cho vay ít nhất 10% vốn góp của chủ sở hữu tại thời điểm phát sinh giao dịch trong kỳ tính thuế với cá nhân điều hành, kiểm soát doanh nghiệp hoặc với cá nhân thuộc một trong các mối quan hệ gia đình như đã nêu trên.

After identifying the related parties and transactions subject to Decree 132/2020/ND-CP, the next step and also the most important compliance requirement is to prepare and maintain Related Party Transaction Records to demonstrate the application of the arm's length principle.

Quy định về giao dịch liên kết về Hồ sơ xác định giá

Việc chuẩn bị và lưu trữ hồ sơ giao dịch liên kết là yếu tố quan trọng nhất để chứng minh việc tuân thủ quy định về giao dịch liên kết và nguyên tắc độc lập. Đối với những doanh nghiệp chưa có đội ngũ chuyên trách về giao dịch liên kết, giải pháp thuê lập hồ sơ giao dịch liên kết iúp đảm bảo hồ sơ được xây dựng đầy đủ, đúng quy định và sẵn sàng giải trình khi cơ quan thuế thanh tra, kiểm tra.

The 3-level Profile structure is based on the OECD recommendation on BEPS Action 13:

- Hồ sơ quốc gia giao dịch liên kết (Local File): Tập trung vào các giao dịch liên kết cụ thể của đơn vị báo cáo tại Việt Nam, bao gồm phân tích chức năng, tài sản, rủi ro (FAR analysis) và so sánh giá. Đây là hồ sơ bắt buộc đối với hầu hết các doanh nghiệp.

- Hồ sơ toàn cầu (Master File): Cung cấp bức tranh tổng thể về hoạt động kinh doanh toàn cầu của tập đoàn, chiến lược chuyển giá và chuỗi giá trị. Hồ sơ này áp dụng cho các tập đoàn đa quốc gia.

- Báo cáo lợi nhuận liên quốc gia (CbCR – Country-by-Country Report): Áp dụng cho tập đoàn có tổng doanh thu hợp nhất toàn cầu từ 18.000 tỷ đồng trở lên. Cung cấp thông tin tổng hợp về phân bổ thu nhập, thuế đã nộp và hoạt động kinh doanh theo từng quốc gia.

To ensure full compliance with regulations on related-party transactions, enterprises need to pay special attention to strict regulations on deadlines for submitting and storing records as required by tax authorities.

Quy định về giao dịch liên kết xác định thời gian nộp và lưu trữ

Regulations on related-party transactions require businesses to strictly comply with two important timelines to avoid being fined by tax authorities for violations.

- Deadline for Submission of Declaration (Form 01): The Related Party Transaction Declaration (Form 01 according to Decree 132/2020/ND-CP) must be submitted at the same time as the Corporate Income Tax Finalization Declaration.

- Time limit for storing and presenting documents: Complete documents (Local File, Master File) must be prepared and stored at the enterprise before submitting the Corporate Income Tax Finalization Declaration. Enterprises must present documents to the tax authority within 15 working days from the date of receiving the request (or 30 days in special cases).

After mastering the requirements for declaration, preparation and storage of records, the next professional focus of the enterprise is to accurately apply economic methods according to Decree 132/2020/ND-CP to determine the price of related-party transactions according to the independence principle.

Methods of determining transfer pricing

Choosing the right method is key to complying with regulations on related party transactions. According to Decree 132/2020/ND-CP regulating related party transactions, the 5 specific methods for determining the price of related party transactions are as follows:

- Comparable Uncontrolled Price (CUP) method: Compares the selling price of a product or service in an associated transaction with the selling price of an equivalent independent transaction. This is the preferred method if highly reliable comparable data can be found.

- Resale Price Method (RPM): Based on the resale price of the product to an independent party, then subtract the reasonable gross margin of the related party to determine the initial purchase price.

- Cost Plus Method (CPM): Based on the cost of production or service provision, then add a reasonable gross profit margin (Gross Markup) to determine the selling price to the related party.

- Transactional Net Margin Method (TNMM): This is the most common method in practice when applying regulations on related party transactions. It compares the net profit margin of the related party (e.g., Net profit on sales) with the net profit margin of independent parties performing similar functions.

- Profit Split Method (PSM): Applied when the transaction is too complex, involves unique intangible assets, requiring both parties to contribute significant value. The resulting profits are divided based on the relative contribution of each party.

While the correct application of economic methods is fundamental, transfer pricing regulations provide exemptions to reduce the compliance burden for some businesses, while also warning of serious risks such as interest expense manipulation.

Quy định về giao dịch liên kết cho các trường hợp được miễn lập Hồ sơ xác định giá

Enterprises are exempted from preparing Transfer Pricing Documents if they meet one of the following criteria:

- Total revenue generated is under VND 50 billion and total value of all related transactions generated during the period is under VND 30 billion.

- Enterprises have signed an Advance Pricing Agreement (APA)

- Enterprises only carry out simple related transactions,No revenue or expenses from exploitation and use of intangible assets, with revenue under VND 200 billion.

See also: Miễn lập hồ sơ giao dịch liên kết.

Tuy nhiên, ngay cả khi được miễn lập Hồ sơ xác định giá giao dịch liên kết, doanh nghiệp vẫn phải đối mặt với một quy định nghiêm ngặt khác trong các quy định về giao dịch liên kết liên quan đến cấu trúc tài chính, đó là khống chế chi phí lãi vay.

Quy định về giao dịch liên kết Khống chế chi phí lãi vay 30% EBITDA

A key point of the regulation on related-party transactions under Decree 132/2020/ND-CP is the control of deductible interest expenses when calculating corporate income tax. Total net interest expenses (after deducting deposit interest and loan interest) exceeding 30% of EBITDA (Earnings before tax, interest, depreciation and amortization) will be excluded from deductible expenses. This is one of the biggest barriers that businesses with related-party relationships have to face.

Các lỗi thường gặp khi doanh nghiệp không tuân thủ quy định giao dịch liên kết

In practice, many businesses still encounter common errors when declaring and preparing related-party transaction records, leading to the risk of being subject to tax arrears or administrative penalties:

- Missing or failing to declare information on related party transactions: Many businesses omit transactions between related parties in their corporate income tax returns, making their records incomplete and causing suspicion from tax authorities.

- Failure to file or incomplete documentation: Lack of Local file, Master file or CbCR is one of the serious errors. Even if the file is filed, if the information is not detailed and there is no transparent comparison database, the enterprise can still be subject to transfer pricing adjustments.

- Using the wrong method to determine transfer pricing: Enterprises apply methods that are not suitable to the nature of the transaction or comparable data, leading to declared prices that are far from the market price principle (Arm's Length Principle), increasing the possibility of being subject to tax arrears.

Seemingly small errors in related party transaction records can expose businesses to significant tax risks. Therefore, understanding the penalty levels and collection mechanisms is an important step to help businesses proactively prevent and comply with the law.

How are businesses punished when they violate regulations on related transactions?

According to the provisions of Decree 125/2020/ND-CP, các mức phạt đối với các vi phạm về thời gian lập và nộp hồ sơ giao dịch liên kết như sau.

Phạt tiền từ 8.000.000 đồng đến 15.000.000 đồng đối với một trong các hành vi say đây:

- Submitting tax declaration documents 61 to 90 days past the prescribed deadline;

- Submitting tax declaration documents 91 days or more after the prescribed deadline but no tax payable arises;

- Not submitting tax return but no tax payable;

- Failure to submit appendices as prescribed in tax management regulations for enterprises with related transactions attached to corporate income tax settlement dossiers.

Phạt tiền từ 15.000.000 đồng đến 25.000.000 đồng đối với hành vi nộp hồ sơ quá thời hạn trên 90 ngày kể từ ngày hết hạn nộp hồ sơ khai thuế, có phát sinh số thuế phải nộp và người nộp thuế đã nộp đủ số tiền thuế, tiền chậm nộp vào ngân sách nhà nước trước thời điểm cơ quan thuế công bố quyết định kiểm tra thuế, thanh tra thuế hoặc trước thời điểm cơ quan thuế lập biên bản về hành vi chậm nộp hồ sơ khai thuế theo quy định.

In addition, if an enterprise fails to submit a dossier of related-party transactions or intentionally fails to fulfill its obligation to declare within the time limit for preparing and submitting a dossier of related-party transactions, the penalty will be very severe. According to the law on tax administration, an enterprise may be fined based on the percentage of the under-declared tax, usually 20% of the under-declared tax due to the act of not declaring or making incorrect declarations leading to a lack of tax obligations. In addition, if the tax authority determines that there are signs of tax evasion, the penalty may be increased to 1-3 times the amount of tax evaded, along with additional collection and late payment fees.

Giải đáp thắc mắc quy định về giao dịch liên kết

Có. Nhiều doanh nghiệp cho rằng chỉ doanh nghiệp FDI mới phải kê khai giao dịch liên kết. Tuy nhiên, bất kỳ doanh nghiệp nào phát sinh giao dịch với bên có quan hệ liên kết theo Nghị định 132 đều phải kê khai, bất kể là doanh nghiệp trong nước hay doanh nghiệp có vốn đầu tư nước ngoài.

Có thể phải lập. Việc lập hồ sơ giao dịch liên kết không phụ thuộc vào việc doanh nghiệp lãi hay lỗ mà phụ thuộc vào việc doanh nghiệp có phát sinh giao dịch với bên liên kết và có thuộc trường hợp miễn trừ hay không. Doanh nghiệp báo lỗ nhiều năm liên tiếp thường là đối tượng được cơ quan thuế chú trọng thanh tra giao dịch liên kết.

Tổng chi phí lãi vay thuần được trừ khi xác định thu nhập chịu thuế không được vượt quá 30% EBITDA. Phần chi phí lãi vay vượt mức 30% EBITDA sẽ không được tính vào chi phí được trừ trong kỳ tính thuế nhưng được chuyển sang các năm tiếp theo theo quy định hiện hành.

Có. Các khoản vay giữa doanh nghiệp và công ty mẹ thuộc giao dịch liên kết. Doanh nghiệp phải kê khai đầy đủ thông tin khoản vay, lãi vay và đánh giá mức lãi suất theo nguyên tắc giá thị trường. Đây là một trong những giao dịch thường xuyên được cơ quan thuế rà soát khi thanh tra chuyển giá.

Cơ quan thuế thường đánh giá dựa trên: Mức độ tăng trưởng doanh thu và lợi nhuận, Tình trạng lỗ liên tục nhiều năm, Biên lợi nhuận thấp bất thường, Chi phí bản quyền, phí dịch vụ nội bộ hoặc lãi vay lớn, Giao dịch với các bên liên kết tại quốc gia có thuế suất thấp và Hồ sơ xác định giá giao dịch liên kết không đầy đủ hoặc không nhất quán.

Doanh nghiệp có thể bị truy thu thuế khi: Xác định giá giao dịch liên kết không theo nguyên tắc độc lập, Không chứng minh được cơ sở xác định giá, Không lập hoặc không xuất trình hồ sơ giao dịch liên kết, Kê khai thiếu doanh thu hoặc tăng chi phí không phù hợp với bản chất giao dịch. Ngoài số thuế bị truy thu, doanh nghiệp còn phải nộp tiền chậm nộp và có thể bị xử phạt vi phạm hành chính.Doanh nghiệp nội địa có phải kê khai giao dịch liên kết không?

Không phát sinh lợi nhuận có phải lập hồ sơ giao dịch liên kết không?

Chi phí lãi vay bị khống chế như thế nào theo Nghị định 132?

Doanh nghiệp chỉ vay vốn từ công ty mẹ có phải kê khai giao dịch liên kết không?

Cơ quan thuế kiểm tra giao dịch liên kết dựa trên những tiêu chí nào?

Doanh nghiệp bị truy thu thuế trong trường hợp nào?

Conclusion and recommendations

Compliance with regulations on related party transactions is not only a legal obligation but also a key factor in protecting businesses from tax and legal risks. In the context of tax authorities increasingly strengthening inspections and examinations of transfer prices, every small error in records or declarations can lead to tax arrears, late payment penalties and affect the reputation of businesses.

Nếu doanh nghiệp đang cần hỗ trợ rà soát, lập hồ sơ hoặc tư vấn tuân thủ quy định giao dịch liên kết, liên hệ ngay với MAN – Master Accountant Network để được hướng dẫn chi tiết, chính xác và phù hợp với thực tế hoạt động.

Contact information MAN – Master Accountant Network

- Address: No. 19A, Street 43, Tan Thuan Ward, Ho Chi Minh City

- Mobile/Zalo: 0903 963 163 – 0903 428 622

- Email: man@man.net.vn

Content production by: Mr. Lê Hoàng Tuyên – Sáng lập viên (Founder) & CEO MAN – Master Accountant Network, Kiểm toán viên CPA Việt Nam với hơn 30 năm kinh nghiệm trong ngành Kế toán, Kiểm toán và Tư vấn Tài chính.